What if the financial trauma of a wallet drain or a lost private key could be partially mitigated by the very agency you usually fear? While the Canada Revenue Agency (CRA) has not issued a dedicated handbook for digital theft, the general rules for capital property suggest that your missing assets may qualify as a disposition at zero value. For many Canadian investors, the shock of a hack is often followed by a second wave of anxiety regarding lost or stolen crypto tax treatment and the potential for a grueling audit. You shouldn't have to pay taxes on wealth that no longer exists; however, the burden of proof rests entirely on your shoulders.

We understand that recovering from a security breach requires both emotional resilience and technical precision. This guide empowers you to transform a devastating loss into a legitimate tax advantage by navigating the CRA's complex reporting requirements for the 2026 filing season. You'll learn how to substantiate your claims with the exact documentation needed to withstand scrutiny and how the 2026 inclusion rate changes affect your recovery strategy. We will break down the definition of permanent loss, the necessity of a defensible audit trail, and the specific steps required to claim a capital loss that protects your remaining portfolio.

Key Takeaways

- Recognize how the CRA treats lost or stolen assets as a 'disposition' at a zero-dollar value, which allows you to legally claim a capital loss.

- Master the nuances of lost or stolen crypto tax treatment to ensure your filing remains compliant while proactively minimizing your 2026 tax liability.

- Identify the specific on-chain evidence, including Transaction IDs and historical wallet logs, required to prove to the CRA that your assets are truly irrecoverable.

- Follow a structured methodology to calculate your Adjusted Cost Base and document the Fair Market Value at the exact time of the security breach.

- Understand why professional oversight is essential for converting complex blockchain data into the defensible, audit-ready records that protect your financial interests.

Lost or Stolen Crypto Tax Treatment: The CRA Framework

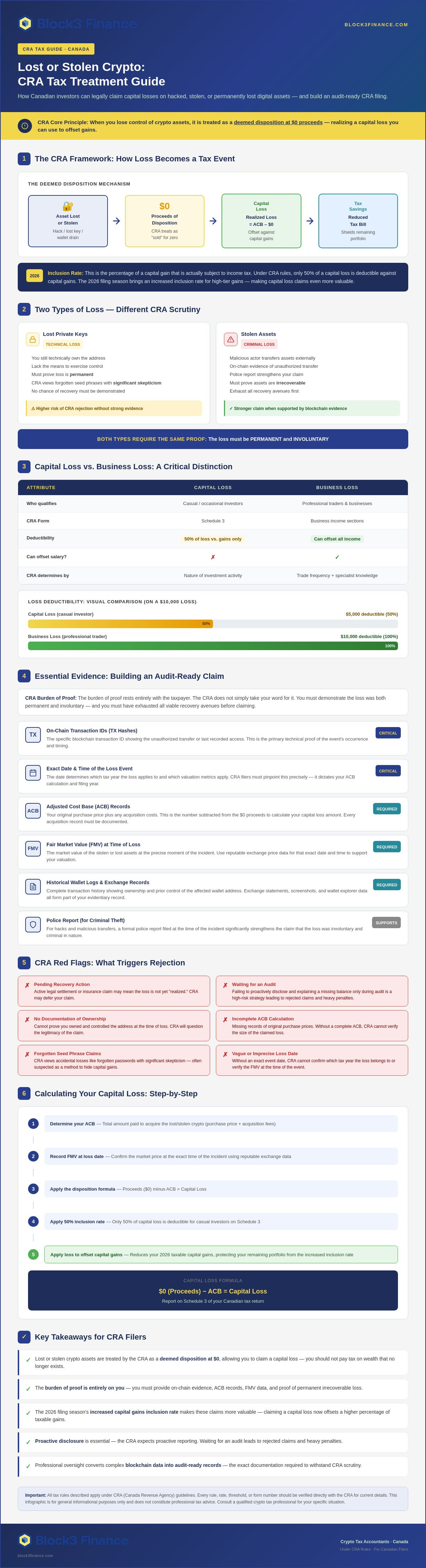

The 2026 tax landscape in Canada demands a more sophisticated approach to reporting digital asset discrepancies than ever before. While the Canada Revenue Agency (CRA) has not yet released a bespoke tax form specifically for blockchain security breaches, the foundation for lost or stolen crypto tax treatment lies in the established principles of capital property disposition. Effectively, when you lose control of your assets, the CRA views this as a deemed disposition. You're essentially "selling" your crypto for proceeds of zero dollars. This mechanism allows you to realize a capital loss, which can then be used to offset capital gains, potentially shielding your remaining portfolio from the 2026 increase in the inclusion rate, which is the specific percentage of a capital gain that is actually subject to income tax, for high-tier gains.

Pinpointing the exact date of the loss is the first step toward building a defensible claim. For CRA filers, the timing of the event dictates which tax year the loss applies to and which valuation metrics are used to calculate the Adjusted Cost Base (ACB). This process is influenced by the global legal status of cryptocurrencies, as international regulatory shifts often dictate how Canadian authorities interpret the legitimacy of specific theft events. In 2026, the CRA expects proactive disclosure. Waiting for an audit to explain a missing balance is a high-risk strategy that often leads to rejected claims and heavy penalties.

Lost Private Keys vs. Stolen Assets

The CRA distinguishes between technical losses and criminal theft based on the permanence of the event. If you've lost your private keys, you still technically own the address, but you lack the means to exercise control. This is a technical loss. Conversely, if a malicious actor transfers your assets to an external wallet, it's a criminal loss. In both scenarios, you must prove the loss is permanent. If there's any chance of recovery, the CRA may deny the disposition. You need to demonstrate that the assets are irrecoverable to satisfy the requirements for a zero-dollar sale. Our crypto tax accountant Canada team specializes in documenting these nuances to ensure your records meet the highest standards of evidence.

Capital Loss vs. Business Expense

Your "intent" at the time of acquisition determines how the loss is categorized on your return. Most casual investors will report the loss on Schedule 3 as a capital loss. Under Canadian rules, only 50% of a capital loss is deductible against capital gains. However, if you're a professional trader or your activity constitutes a business, you might qualify for a business loss deduction. This is more advantageous because business losses can often offset other sources of income, such as your salary. The CRA looks at the frequency of your trades and your level of specialized knowledge to determine your status. It's a high-stakes distinction that requires a disciplined analysis of your trading history before you file your 2026 return.

How the CRA Evaluates Claims for Lost Digital Assets

Navigating the CRA's scrutiny requires more than a police report; it demands an airtight evidentiary chain. The Agency operates on the principle that the burden of proof rests entirely with the taxpayer. When you assert a claim regarding lost or stolen crypto tax treatment, the CRA doesn't simply take your word for it. They view "accidental" losses, such as forgotten seed phrases or discarded hardware, with significant skepticism. To the Agency, these often look like convenient excuses to hide capital gains or manufacture artificial losses. You must demonstrate that the loss was both permanent and involuntary to satisfy the requirements for a capital loss claim.

According to the CRA's digital currency tax guidance, your records must clearly support the value and ownership of the assets in question. A critical factor in 2026 is the "reasonable expectation of recovery." If you're pursuing a legal settlement or an insurance claim, the CRA may argue the loss isn't yet realized. They want to see that you've exhausted all viable avenues for retrieval before they allow you to write off the asset value. If you find yourself struggling to organize these high-stakes details, you can consult with our team to ensure your submission is defensible.

The 'Proof of Ownership' Requirement

The CRA requires you to link your legal identity to the specific wallet address involved in the loss. This is often difficult for decentralized wallets that don't have KYC (Know Your Customer) data. You must bridge this gap by providing historical purchase records from exchanges that show the initial acquisition and the subsequent transfer to your self-custody wallet. Maintaining pristine blockchain financial records is the only way to prove you were the beneficial owner before the security breach occurred. Without this trail, the CRA may disqualify the loss entirely.

The 'Involuntary' Nature of the Loss

The Agency distinguishes between a scam, where you might have voluntarily sent funds to a fraudulent party, and theft, where funds were moved without your consent. Sending crypto to a "fat-finger" wrong address generally doesn't qualify as a capital loss; the CRA often views this as a personal mistake rather than a disposition of property. However, involuntary events like phishing attacks, smart contract exploits, or exchange bankruptcies are more likely to be accepted. In the case of exchange collapses, the loss may be treated as a bad debt claim under specific sections of the Income Tax Act, provided you can prove the debt is truly uncollectible.

Proving Your Loss: Essential Evidence for 2026 CRA Filers

Proving a loss to the CRA requires more than just an entry in a spreadsheet. It demands a comprehensive evidentiary package that mirrors the technical complexity of the assets themselves. For those seeking favorable lost or stolen crypto tax treatment, the primary objective is to provide an undeniable link between the security breach and the resulting financial deficit. This starts with on-chain evidence. Transaction IDs (TXIDs) serve as the digital fingerprints of the blockchain, providing a timestamped record of the unauthorized movement of funds. By documenting these TXIDs alongside your public keys and historical activity logs, you create a baseline of ownership and control that existed prior to the event.

The CRA's Guide for Cryptocurrency Users emphasizes that taxpayers must maintain records that support their tax positions. In cases of theft, this includes filing a report with local law enforcement or the Canadian Anti-Fraud Centre (CAFC). While police may not always recover the assets, the existence of an official report validates your claim that the loss was involuntary. You should also archive all correspondence with exchanges or wallet providers. These communications often contain technical acknowledgments of vulnerabilities or security failures that support your narrative during an audit.

Blockchain Forensics as a Tax Tool

Modern tax preparation often involves tracing stolen funds through block explorers to their final destination. If your assets were moved to a known "mixer" or a centralized exchange, documenting this path proves you no longer have access. A narrative summary of the hack provides context for CRA auditors, explaining exactly how the exploit occurred. Utilizing specialized crypto audit preparation ensures that these forensic details are presented in a language that tax authorities understand, bridging the gap between complex on-chain data and formal financial reporting.

Third-Party Verification and Reports

Reporting to the CAFC is a critical step for 2026 filers because it creates a third-party record of the illicit activity. For protocol-level exploits, obtaining statements from security firms or the project's official post-mortem report adds a layer of institutional credibility to your claim. In 2026, the 'Reasonable Effort' standard requires taxpayers to demonstrate they've taken all logically available steps to report the crime, track the assets, and secure their remaining infrastructure before claiming a capital loss. This comprehensive approach transforms a chaotic security breach into a disciplined, audit-ready tax position that protects your broader financial interests.

Reporting the Loss on Your 2026 Canadian Tax Return

Executing the final stage of your financial recovery involves synthesizing your evidence into a formal filing that stands up to Agency scrutiny. For CRA filers, this requires a precise four-step workflow. First, calculate the Adjusted Cost Base (ACB) of the missing assets, which represents the total historical cost including acquisition fees. Second, establish the Fair Market Value (FMV) at the time of the loss as zero dollars. This deemed disposition effectively creates the capital loss on your ledger. Third, record the transaction on Schedule 3 for personal investments. Finally, you must retain all supporting documentation for the mandatory six-year period. While this guide provides a strategic framework, taxpayers should verify all specific figures and deadlines directly with the Canada Revenue Agency (CRA) to ensure their 2026 submission is accurate.

Calculating your ACB across multiple wallets requires the weighted average cost method, which is the mandatory accounting practice of averaging the purchase price of all identical tokens in your portfolio to determine a single cost basis for that specific asset class. This prevents you from "cherry-picking" specific high-cost units to inflate your loss. By applying this method, you create a transparent and mathematically sound record of your lost or stolen crypto tax treatment. Precision here is vital; an error in your cost basis calculation can lead to the disqualification of your entire claim during a subsequent review.

Schedule 3 vs. T2125

Determining the correct form is as important as the numbers themselves. Most Canadians report their losses on Schedule 3, where only 50% of the loss is deductible against capital gains. However, if your activity is classified as a business, you must use Form T2125 to claim a business loss, allowing a 100% deduction against all income sources. Misidentifying your trading status is one of the crypto tax mistakes that often triggers an audit. We recommend consulting the CRA's latest bulletins to confirm your status before filing.

Deadlines and Penalties

For the 2025 tax year, the general filing deadline is April 30, 2026, while self-employed individuals have until June 15, 2026. Note that all tax payments remain due by April 30 regardless of your filing category. If your loss claim is denied due to poor documentation, you may face back taxes and compounding interest. Understanding the gravity of CRA penalties and risks is essential for maintaining your financial standing. To navigate these complexities with professional oversight, reach out to our specialists for a comprehensive review of your 2026 tax position.

Defensible Records: How Block3 Finance Secures Your Claims

Automated tax software serves as a useful data aggregator, but it lacks the intellectual depth to construct a defensible narrative for the CRA. When dealing with lost or stolen crypto tax treatment, these platforms often categorize missing assets as simple withdrawals or errors, which can inadvertently trigger red flags during a compliance review. Block3 Finance operates at a different level. We specialize in turning chaotic, fragmented on-chain data into clean, audit-ready books that reflect the legal and financial reality of your situation. Our methodology moves beyond simple calculation; we provide the forensic substantiation that proves your loss was involuntary and permanent.

For high-net-worth individuals and corporate entities, a security breach is a systemic threat. Our strategic CFO services offer a high-level roadmap for navigating these crises, ensuring that your tax strategy aligns with your long-term wealth preservation goals. By engaging a crypto tax accountant in Canada, you secure professional representation that understands the specific nuances of the 2026 reporting environment. We bridge the gap between the technical reality of the blockchain and the administrative requirements of the Agency, resolving friction before it escalates into a legal dispute.

Expert Audit Representation

We don't just file reports; we defend them. If the CRA initiates an inquiry into your capital loss claims, our team steps in to lead the communication. With 13+ years of blockchain financial expertise, we possess the technical rigor to explain complex exploits to auditors who may lack deep crypto knowledge. This advocacy shifts your position from a defensive posture to one of total command. It ensures that your 2026 filing is treated with the professional respect it deserves, backed by a firm that has been at the forefront of digital asset accounting since the industry's infancy.

Proactive Compliance for the Future

Recovery is only the first step toward reclaiming your financial agency. True mastery of your portfolio requires implementing robust security protocols and meticulous tracking for your remaining assets. Our monthly accounting and bookkeeping services ensure that no data gaps exist, making future filings seamless and highly resilient. We help you move past the trauma of theft by building a disciplined foundation for growth. Don't leave your financial standing to chance in a volatile landscape. Contact us for a professional consultation to secure your claims and build a resilient tax strategy for 2026 and beyond.

Reclaiming Financial Command in the 2026 Tax Landscape

Transforming the trauma of a security breach into a strategic tax advantage is the final step in your recovery journey. By mastering the nuances of lost or stolen crypto tax treatment, you ensure that your 2026 filing reflects the reality of your portfolio rather than a phantom gain. You've learned that a successful capital loss claim rests on three pillars: establishing beneficial ownership, documenting the involuntary nature of the event, and maintaining a forensic audit trail that satisfies the CRA's rigorous evidentiary standards. These steps move you from a defensive posture to one of total command over your financial future.

Navigating these high-stakes regulations requires a partner with the technical rigor to bridge the gap between blockchain data and Canadian tax law. As the firm ranked #1 Crypto Tax Provider by Bitcoin.com, Block3 Finance provides specialized CRA compliance and global expertise with a local Ontario presence. We turn chaotic on-chain history into defensible records that protect your remaining wealth. Secure your crypto tax claim with Block3 Finance's expert Canadian filing services and file with the confidence that comes from professional advocacy. Your financial agency is within reach, and we're ready to help you reclaim it.

Frequently Asked Questions

Can I claim a capital loss for crypto I sent to the wrong wallet address?

Generally, you cannot claim a capital loss for funds sent to an incorrect address. The CRA typically classifies these events as personal mistakes rather than involuntary dispositions of property. To qualify for a loss, the event must be beyond your control, such as a hack or a security breach. Since you voluntarily initiated the transaction, it doesn't meet the Agency's threshold for an involuntary loss of capital property.

What evidence does the CRA require for a stolen crypto claim in 2026?

For 2026 filers, the CRA demands a comprehensive evidentiary package including Transaction IDs (TXIDs), public keys, and historical wallet logs. You must also provide third-party verification, such as a report from the Canadian Anti-Fraud Centre (CAFC), to substantiate the involuntary nature of the event. Mastering the nuances of lost or stolen crypto tax treatment requires you to bridge the gap between technical on-chain data and the Agency's formal reporting requirements.

Is there a limit to how much stolen crypto I can write off in Canada?

There is no specific dollar limit on the amount of capital loss you can report. However, you can only use 50% of your capital loss to offset 50% of your capital gains. If your losses exceed your gains for the year, you can carry the excess back three years or forward indefinitely under CRA rules. This allows you to shield future gains from taxation, providing a long-term mechanism for financial recovery.

What happens if I recover my stolen crypto in a later tax year?

If you regain control of assets previously reported as a loss, you must treat the recovery as a capital gain in the year it occurs. Since you already realized the loss at a zero-dollar value, the recovered assets will generally have an adjusted cost base of zero. This ensures your tax records remain balanced and compliant with current regulations while reflecting the restoration of your wealth.

Do I need a police report to claim a crypto theft loss on my Canadian taxes?

While the Income Tax Act doesn't explicitly mandate a police report, it is a critical component of a defensible claim for lost or stolen crypto tax treatment. The CRA often views undocumented losses with skepticism, suspecting they might be hidden transfers. An official report serves as vital evidence that the theft was a criminal event rather than a voluntary transfer or an attempt to manufacture a tax deduction.

Can I deduct losses from a crypto exchange bankruptcy or 'rug pull'?

Yes, you can often deduct these losses, though the specific reporting method depends on the event's nature. Rug pulls are generally reported as capital losses on Schedule 3 because the assets have become worthless. Exchange bankruptcies may qualify as bad debts under specific sections of the Income Tax Act, requiring you to prove the debt is truly uncollectible before claiming the deduction on your return.

How do I calculate the value of my loss if the token price has changed?

Your loss is determined by your Adjusted Cost Base (ACB), which is the historical cost you paid to acquire the assets. You don't use the market price at the time of the theft to calculate the loss. The calculation involves subtracting your proceeds of disposition, which is zero in a theft scenario, from your original acquisition cost. This ensures you're only writing off the capital you actually invested.

Is losing my private keys considered a 'casualty loss' by the CRA?

The term 'casualty loss' is a US-specific concept and does not apply to CRA filers. In Canada, losing your private keys is treated as a deemed disposition of capital property at zero value. You must provide rigorous proof that the keys are permanently lost and the assets are irrecoverable to satisfy the CRA that a genuine disposition has occurred, allowing you to realize the capital loss.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Block3 Finance, with over 26+ years of Canadian and international tax and accounting experience. A crypto accounting specialist since the early days of Bitcoin, he has consulted for over 38 crypto companies and collaborated with legal professionals on regulatory matters. His expertise spans corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, and CRA audits.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Block3 Finance and Tax Partners has 44 full-time accountants and over 9,800+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances.

Frequently Asked Questions

Lost Private Keys vs. Stolen Assets

The CRA distinguishes between technical losses and criminal theft based on the permanence of the event. If you've lost your private keys, you still technically own the address, but you lack the means to exercise control. This is a technical loss. Conversely, if a malicious actor transfers your assets to an external wallet, it's a criminal loss. In both scenarios, you must prove the loss is permanent. If there's any chance of recovery, the CRA may deny the disposition. You need to demonstrate that the assets are irrecoverable to satisfy the requirements for a zero-dollar sale. Our crypto tax accountant Canada team specializes in documenting these nuances to ensure your records meet the highest standards of evidence.

Capital Loss vs. Business Expense

Your "intent" at the time of acquisition determines how the loss is categorized on your return. Most casual investors will report the loss on Schedule 3 as a capital loss. Under Canadian rules, only 50% of a capital loss is deductible against capital gains. However, if you're a professional trader or your activity constitutes a business, you might qualify for a business loss deduction. This is more advantageous because business losses can often offset other sources of income, such as your salary. The CRA looks at the frequency of your trades and your level of specialized knowledge to determine your status. It's a high-stakes distinction that requires a disciplined analysis of your trading history before you file your 2026 return. Navigating the CRA's scrutiny requires more than a police report; it demands an airtight evidentiary chain. The Agency operates on the principle that the burden of proof rests entirely with the taxpayer. When you assert a claim regarding lost or stolen crypto tax treatment, the CRA doesn't simply take your word for it. They view "accidental" losses, such as forgotten seed phrases or discarded hardware, with significant skepticism. To the Agency, these often look like convenient excuses to hide capital gains or manufacture artificial losses. You must demonstrate that the loss was both permanent and involuntary to satisfy the requirements for a capital loss claim. According to the CRA's digital currency tax guidance, your records must clearly support the value and ownership of the assets in question. A critical factor in 2026 is the "reasonable expectation of recovery." If you're pursuing a legal settlement or an insurance claim, the CRA may argue the loss isn't yet realized. They want to see that you've exhausted all viable avenues for retrieval before they allow you to write off the asset value. If you find yourself struggling to organize these high-stakes details, you can consult with our team to ensure your submission is defensible.

The 'Proof of Ownership' Requirement

The CRA requires you to link your legal identity to the specific wallet address involved in the loss. This is often difficult for decentralized wallets that don't have KYC (Know Your Customer) data. You must bridge this gap by providing historical purchase records from exchanges that show the initial acquisition and the subsequent transfer to your self-custody wallet. Maintaining pristine blockchain financial records is the only way to prove you were the beneficial owner before the security breach occurred. Without this trail, the CRA may disqualify the loss entirely.

The 'Involuntary' Nature of the Loss

The Agency distinguishes between a scam, where you might have voluntarily sent funds to a fraudulent party, and theft, where funds were moved without your consent. Sending crypto to a "fat-finger" wrong address generally doesn't qualify as a capital loss; the CRA often views this as a personal mistake rather than a disposition of property. However, involuntary events like phishing attacks, smart contract exploits, or exchange bankruptcies are more likely to be accepted. In the case of exchange collapses, the loss may be treated as a bad debt claim under specific sections of the Income Tax Act, provided you can prove the debt is truly uncollectible. Proving a loss to the CRA requires more than just an entry in a spreadsheet. It demands a comprehensive evidentiary package that mirrors the technical complexity of the assets themselves. For those seeking favorable lost or stolen crypto tax treatment, the primary objective is to provide an undeniable link between the security breach and the resulting financial deficit. This starts with on-chain evidence. Transaction IDs (TXIDs) serve as the digital fingerprints of the blockchain, providing a timestamped record of the unauthorized movement of funds. By documenting these TXIDs alongside your public keys and historical activity logs, you create a baseline of ownership and control that existed prior to the event. The CRA's Guide for Cryptocurrency Users emphasizes that taxpayers must maintain records that support their tax positions. In cases of theft, this includes filing a report with local law enforcement or the Canadian Anti-Fraud Centre (CAFC). While police may not always recover the assets, the existence of an official report validates your claim that the loss was involuntary. You should also archive all correspondence with exchanges or wallet providers. These communications often contain technical acknowledgments of vulnerabilities or security failures that support your narrative during an audit.

Blockchain Forensics as a Tax Tool

Modern tax preparation often involves tracing stolen funds through block explorers to their final destination. If your assets were moved to a known "mixer" or a centralized exchange, documenting this path proves you no longer have access. A narrative summary of the hack provides context for CRA auditors, explaining exactly how the exploit occurred. Utilizing specialized crypto audit preparation ensures that these forensic details are presented in a language that tax authorities understand, bridging the gap between complex on-chain data and formal financial reporting.

Third-Party Verification and Reports

Reporting to the CAFC is a critical step for 2026 filers because it creates a third-party record of the illicit activity. For protocol-level exploits, obtaining statements from security firms or the project's official post-mortem report adds a layer of institutional credibility to your claim. In 2026, the 'Reasonable Effort' standard requires taxpayers to demonstrate they've taken all logically available steps to report the crime, track the assets, and secure their remaining infrastructure before claiming a capital loss. This comprehensive approach transforms a chaotic security breach into a disciplined, audit-ready tax position that protects your broader financial interests. Executing the final stage of your financial recovery involves synthesizing your evidence into a formal filing that stands up to Agency scrutiny. For CRA filers, this requires a precise four-step workflow. First, calculate the Adjusted Cost Base (ACB) of the missing assets, which represents the total historical cost including acquisition fees. Second, establish the Fair Market Value (FMV) at the time of the loss as zero dollars. This deemed disposition effectively creates the capital loss on your ledger. Third, record the transaction on Schedule 3 for personal investments. Finally, you must retain all supporting documentation for the mandatory six-year period. While this guide provides a strategic framework, taxpayers should verify all specific figures and deadlines directly with the Canada Revenue Agency (CRA) to ensure their 2026 submission is accurate. Calculating your ACB across multiple wallets requires the weighted average cost method, which is the mandatory accounting practice of averaging the purchase price of all identical tokens in your portfolio to determine a single cost basis for that specific asset class. This prevents you from "cherry-picking" specific high-cost units to inflate your loss. By applying this method, you create a transparent and mathematically sound record of your lost or stolen crypto tax treatment. Precision here is vital; an error in your cost basis calculation can lead to the disqualification of your entire claim during a subsequent review.

Schedule 3 vs. T2125

Determining the correct form is as important as the numbers themselves. Most Canadians report their losses on Schedule 3, where only 50% of the loss is deductible against capital gains. However, if your activity is classified as a business, you must use Form T2125 to claim a business loss, allowing a 100% deduction against all income sources. Misidentifying your trading status is one of the crypto tax mistakes that often triggers an audit. We recommend consulting the CRA's latest bulletins to confirm your status before filing.

Deadlines and Penalties

For the 2025 tax year, the general filing deadline is April 30, 2026, while self-employed individuals have until June 15, 2026. Note that all tax payments remain due by April 30 regardless of your filing category. If your loss claim is denied due to poor documentation, you may face back taxes and compounding interest. Understanding the gravity of CRA penalties and risks is essential for maintaining your financial standing. To navigate these complexities with professional oversight, reach out to our specialists for a comprehensive review of your 2026 tax position. Automated tax software serves as a useful data aggregator, but it lacks the intellectual depth to construct a defensible narrative for the CRA. When dealing with lost or stolen crypto tax treatment, these platforms often categorize missing assets as simple withdrawals or errors, which can inadvertently trigger red flags during a compliance review. Block3 Finance operates at a different level. We specialize in turning chaotic, fragmented on-chain data into clean, audit-ready books that reflect the legal and financial reality of your situation. Our methodology moves beyond simple calculation; we provide the forensic substantiation that proves your loss was involuntary and permanent. For high-net-worth individuals and corporate entities, a security breach is a systemic threat. Our strategic CFO services offer a high-level roadmap for navigating these crises, ensuring that your tax strategy aligns with your long-term wealth preservation goals. By engaging a crypto tax accountant in Canada, you secure professional representation that understands the specific nuances of the 2026 reporting environment. We bridge the gap between the technical reality of the blockchain and the administrative requirements of the Agency, resolving friction before it escalates into a legal dispute.

Expert Audit Representation

We don't just file reports; we defend them. If the CRA initiates an inquiry into your capital loss claims, our team steps in to lead the communication. With 13+ years of blockchain financial expertise, we possess the technical rigor to explain complex exploits to auditors who may lack deep crypto knowledge. This advocacy shifts your position from a defensive posture to one of total command. It ensures that your 2026 filing is treated with the professional respect it deserves, backed by a firm that has been at the forefront of digital asset accounting since the industry's infancy.

Proactive Compliance for the Future

Recovery is only the first step toward reclaiming your financial agency. True mastery of your portfolio requires implementing robust security protocols and meticulous tracking for your remaining assets. Our monthly accounting and bookkeeping services ensure that no data gaps exist, making future filings seamless and highly resilient. We help you move past the trauma of theft by building a disciplined foundation for growth. Don't leave your financial standing to chance in a volatile landscape. Contact us for a professional consultation to secure your claims and build a resilient tax strategy for 2026 and beyond. Transforming the trauma of a security breach into a strategic tax advantage is the final step in your recovery journey. By mastering the nuances of lost or stolen crypto tax treatment, you ensure that your 2026 filing reflects the reality of your portfolio rather than a phantom gain. You've learned that a successful capital loss claim rests on three pillars: establishing beneficial ownership, documenting the involuntary nature of the event, and maintaining a forensic audit trail that satisfies the CRA's rigorous evidentiary standards. These steps move you from a defensive posture to one of total command over your financial future. Navigating these high-stakes regulations requires a partner with the technical rigor to bridge the gap between blockchain data and Canadian tax law. As the firm ranked #1 Crypto Tax Provider by Bitcoin.com, Block3 Finance provides specialized CRA compliance and global expertise with a local Ontario presence. We turn chaotic on-chain history into defensible records that protect your remaining wealth. Secure your crypto tax claim with Block3 Finance's expert Canadian filing services and file with the confidence that comes from professional advocacy. Your financial agency is within reach, and we're ready to help you reclaim it.

Can I claim a capital loss for crypto I sent to the wrong wallet address?

Generally, you cannot claim a capital loss for funds sent to an incorrect address. The CRA typically classifies these events as personal mistakes rather than involuntary dispositions of property. To qualify for a loss, the event must be beyond your control, such as a hack or a security breach. Since you voluntarily initiated the transaction, it doesn't meet the Agency's threshold for an involuntary loss of capital property.

What evidence does the CRA require for a stolen crypto claim in 2026?

For 2026 filers, the CRA demands a comprehensive evidentiary package including Transaction IDs (TXIDs), public keys, and historical wallet logs. You must also provide third-party verification, such as a report from the Canadian Anti-Fraud Centre (CAFC), to substantiate the involuntary nature of the event. Mastering the nuances of lost or stolen crypto tax treatment requires you to bridge the gap between technical on-chain data and the Agency's formal reporting requirements.

Is there a limit to how much stolen crypto I can write off in Canada?

There is no specific dollar limit on the amount of capital loss you can report. However, you can only use 50% of your capital loss to offset 50% of your capital gains. If your losses exceed your gains for the year, you can carry the excess back three years or forward indefinitely under CRA rules. This allows you to shield future gains from taxation, providing a long-term mechanism for financial recovery.

What happens if I recover my stolen crypto in a later tax year?

If you regain control of assets previously reported as a loss, you must treat the recovery as a capital gain in the year it occurs. Since you already realized the loss at a zero-dollar value, the recovered assets will generally have an adjusted cost base of zero. This ensures your tax records remain balanced and compliant with current regulations while reflecting the restoration of your wealth.

Do I need a police report to claim a crypto theft loss on my Canadian taxes?

While the Income Tax Act doesn't explicitly mandate a police report, it is a critical component of a defensible claim for lost or stolen crypto tax treatment. The CRA often views undocumented losses with skepticism, suspecting they might be hidden transfers. An official report serves as vital evidence that the theft was a criminal event rather than a voluntary transfer or an attempt to manufacture a tax deduction.

Can I deduct losses from a crypto exchange bankruptcy or 'rug pull'?

Yes, you can often deduct these losses, though the specific reporting method depends on the event's nature. Rug pulls are generally reported as capital losses on Schedule 3 because the assets have become worthless. Exchange bankruptcies may qualify as bad debts under specific sections of the Income Tax Act, requiring you to prove the debt is truly uncollectible before claiming the deduction on your return.

How do I calculate the value of my loss if the token price has changed?

Your loss is determined by your Adjusted Cost Base (ACB), which is the historical cost you paid to acquire the assets. You don't use the market price at the time of the theft to calculate the loss. The calculation involves subtracting your proceeds of disposition, which is zero in a theft scenario, from your original acquisition cost. This ensures you're only writing off the capital you actually invested.

Is losing my private keys considered a 'casualty loss' by the CRA?

The term 'casualty loss' is a US-specific concept and does not apply to CRA filers. In Canada, losing your private keys is treated as a deemed disposition of capital property at zero value. You must provide rigorous proof that the keys are permanently lost and the assets are irrecoverable to satisfy the CRA that a genuine disposition has occurred, allowing you to realize the capital loss.