What if the transparency of the public ledger is exactly what puts your organization at risk during a federal examination? Many digital asset enterprises operate under the assumption that on-chain data is inherently audit-ready, yet raw transaction logs are not the same as defensible blockchain financial records. You likely feel the mounting pressure of fragmented data across multiple chains and the constant friction of matching cryptic hashes to fiat-denominated invoices. It's a common frustration to see a disconnect between your real-world operations and the rigid requirements of IRS Form 8949.

We believe that institutional-grade reporting requires more than just a block explorer; it demands a strategic transformation of raw data into a reconciled narrative that justifies your tax positions. This guide provides a clear framework to ensure your organization is fully prepared for the 2026 filing season under IRS rules. You'll learn how to maintain clean books that reflect fair value under ASU 2023-08 and how to navigate the complexities of the new Form 1099-DA. We'll move your reporting from a defensive posture to one of total financial mastery, reducing tax liability through precision and discipline.

Key Takeaways

- Understand the critical distinction between raw transaction hashes and GAAP-compliant blockchain financial records that meet rigorous IRS standards.

- Identify the essential components of an audit-defensible record, including precise Fair Market Value (FMV) calculations at the exact moment of each transaction.

- Resolve the reconciliation gap between on-chain sub-ledgers and traditional accounting software to ensure your general ledger remains accurate and defensible.

- Master the 2026 audit-readiness checklist to streamline monthly wallet reconciliations and ensure proper classification for new reporting requirements under IRS rules.

- Transition from merely managing regulatory friction to achieving total command over your financial landscape through proactive oversight and strategic record-keeping.

Beyond the Ledger: Why Blockchain Data is Not a Financial Record

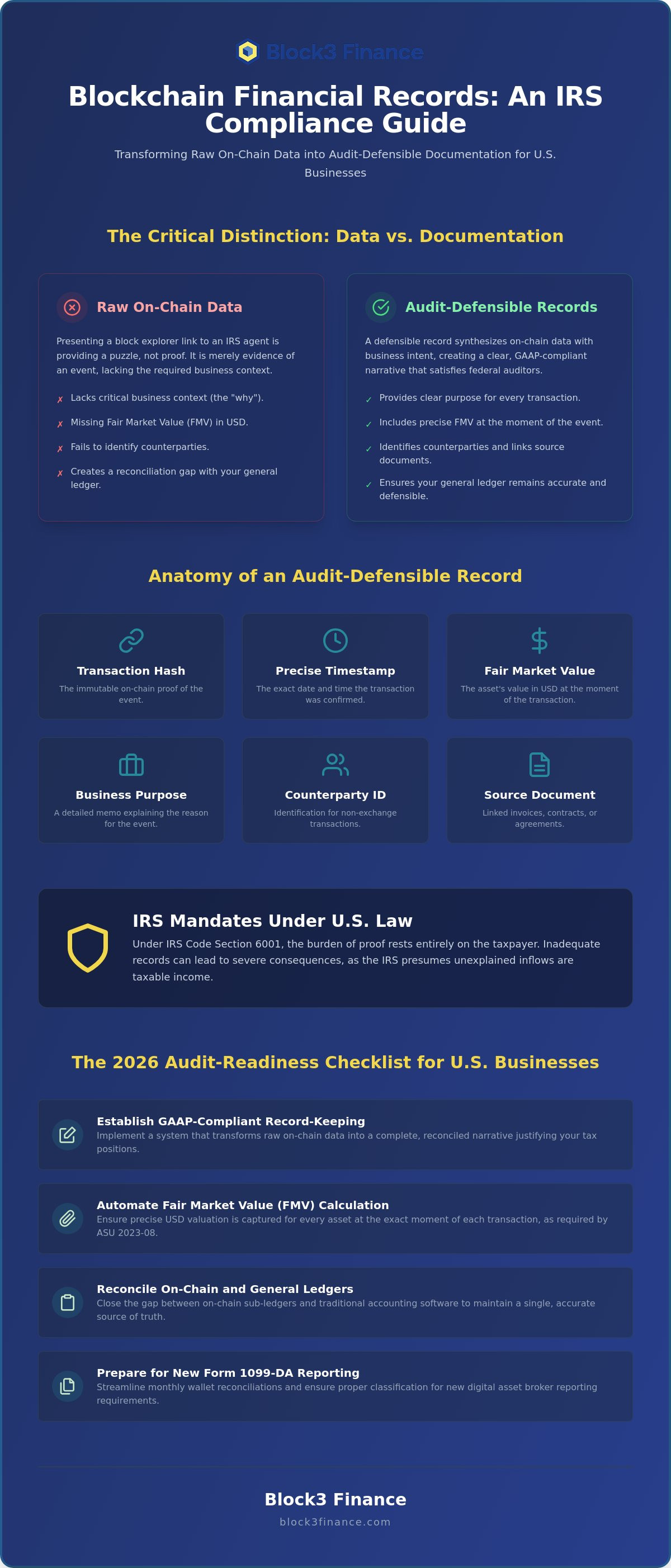

The ledger is a mirror, not a balance sheet. While blockchain technology provides a revolutionary, immutable record of movement, it lacks the commercial context required to satisfy a federal auditor. You must understand that a transaction hash is merely evidence of an event. It's not a complete financial record. To achieve true audit-readiness, you need to bridge the gap between anonymous on-chain activity and the rigorous standards of U.S. tax law. We see many businesses struggle because they mistake data for documentation. This distinction is where your compliance strategy either succeeds or fails.

The IRS doesn't view a block explorer as a substitute for a general ledger. If you present an agent with a list of Etherscan links during an examination, you haven't provided proof; you've provided a puzzle. Creating defensible blockchain financial records requires you to take that raw data and wrap it in business intent. This means identifying the "why" behind the "what." Was that 50 ETH transfer a vendor payment, a shareholder distribution, or a simple internal wallet shuffle? Without this metadata, the IRS is legally permitted to categorize unexplained inflows as taxable income by default. You don't want to leave that narrative to an auditor's discretion.

The Evidence vs. Record Distinction

Defensible blockchain financial records are the synthesis of on-chain data and business intent. Think of the blockchain as the "proof of existence," while your accounting system provides the "proof of characterization." A transaction hash only proves that assets moved from Point A to Point B. It doesn't explain the fair market value at the time of the trade or the tax cost basis of the assets involved. This distinction becomes critical in high-volume environments like DeFi or NFT trading. In these spaces, automated "data noise" can quickly bury meaningful financial activity under thousands of irrelevant smart contract interactions, making manual reconciliation nearly impossible without a structured framework.

IRS Expectations for Digital Asset Documentation

Under IRS rules, specifically Section 6001, every person liable for any tax must keep "permanent books of account or records" that are sufficient to establish the amount of gross income and deductions. The legal burden of proof rests entirely on you, the taxpayer. The IRS increasingly uses sophisticated tools to scrape on-chain data and identify undisclosed income. If your internal documentation doesn't match the public ledger, the discrepancy triggers immediate red flags. You need a robust audit and compliance strategy that transforms anonymous wallet activity into a transparent, GAAP-compliant narrative. This includes maintaining records of:

- Precise timestamps and the corresponding fair market value in USD at the moment of the transaction.

- Detailed memos explaining the specific business purpose for every on-chain event.

- Counterparty identification for transactions that occur outside of centralized exchanges.

- Original source documentation, such as digital invoices or employment contracts, directly linked to the on-chain hash.

By treating the blockchain as a foundational audit trail rather than a finished product, you gain total command over your financial landscape. This proactive stance shifts you from a defensive position of managing regulations to an offensive one focused on growth and institutional stability.

The Anatomy of an Audit-Defensible On-Chain Record

A single transaction hash is a ghost without a body. To transform these digital traces into blockchain financial records that withstand federal scrutiny, you must build a comprehensive data profile for every event. The IRS doesn't just want to see that a transfer occurred; they require proof of the asset's value and the commercial context surrounding it. This means every record must capture the precise timestamp, the fair market value at the moment of receipt, and the associated transaction fees. We believe that mastery over these details is what separates a vulnerable business from one that is truly audit-ready.

Gas fees represent a specific point of friction that many firms overlook. Under IRS rules, these network costs are often deductible business expenses or can be added to the cost basis of an acquired asset. By categorizing gas as a separate line item, you reduce your overall tax liability while demonstrating a high level of accounting rigor. We recommend linking every on-chain hash directly to off-chain documentation, such as digital invoices or vendor contracts, to ensure that the business intent is undeniable. If you find this reconciliation process overwhelming, our monthly accounting services can help streamline the data capture and classification.

Metadata Requirements for IRS Compliance

Your internal ledger must track specific fields to satisfy IRS requirements for digital assets. At a minimum, each entry must include the date, the Fair Market Value (FMV) in USD, the unique Transaction ID, and the involved Wallet Addresses. You also have a strict basis tracking requirement for every individual asset in your inventory. Cost basis is the original value of an asset for tax purposes, adjusted for fees. Maintaining this granularity is the only way to accurately calculate gains or losses when you eventually dispose of the asset, especially as the IRS phases in new cost basis reporting requirements for brokers in 2026.

Fair Value Measurement Under ASU 2023-08

The landscape of crypto accounting is shifting toward greater transparency and accuracy. Starting in 2026, ASU 2023-08 requires many U.S. firms to measure their digital assets at fair value on their financial statements. This represents a significant departure from the old historical cost less impairment model, which often resulted in understated balance sheets. This new requirement ensures that your blockchain financial records reflect the actual economic reality of your holdings at the end of each reporting period. While this improves the quality of your financial data, it also demands more frequent and precise valuation methodologies to stay compliant. For those managing more complex portfolios, our CFO services provide the strategic oversight needed to navigate these evolving standards. If you're concerned about how these changes will impact your next filing, it's wise to consult with our team to review your current reporting framework.

Reconciling Reality: On-Chain Activity vs. General Ledgers

Triple-entry accounting isn't just a conceptual buzzword; it's the operational reality of any hybrid fiat-crypto business model. While the blockchain provides the third entry as a public proof of transaction, your internal General Ledger (GL) remains the ultimate authority for IRS reporting. The friction arises when you attempt to sync these two worlds. We often see automated sub-ledgers fail to map correctly to QuickBooks or Xero, leading to a fragmented view of your financial health. If your systems don't distinguish between a revenue event and a simple internal transfer between company-owned wallets, you risk double-counting income and inflating your tax liability. This oversight doesn't just cost money; it creates a vulnerability that federal auditors are trained to exploit.

A proactive approach to reconciliation is the only way to maintain defensible blockchain financial records. Waiting until year-end to untangle thousands of smart contract interactions is a recipe for disaster. You need a methodical workflow that validates on-chain activity against your bank statements and invoices in real-time. This level of discipline ensures that your books are always ready for scrutiny, shifting you from a defensive posture to one of total command over your financial narrative. We prioritize this continuous verification to resolve discrepancies before they become permanent errors on your tax return.

Bridging the Gap Between Wallets and ERPs

Specialized middleware acts as the vital connective tissue in modern bookkeeping. However, automated data ingestion from exchanges often misses the "why" behind the movement. You might see an inflow but lack the documentation to prove it's a loan repayment rather than sales revenue. This is why manual oversight remains essential. For a deeper look at institutional-grade strategies, explore our guide on digital asset bookkeeping. Relying solely on raw API feeds without human verification often results in misclassified assets and incorrect cost basis tracking, both of which trigger red flags under IRS rules.

Handling Complex On-Chain Events

DeFi activity introduces layers of complexity that traditional accounting software isn't built to handle. Liquidity pool (LP) tokens and wrapped assets require careful tracking of cost basis and fair value to ensure accurate reporting. You must also differentiate between staking rewards, which are generally treated as income upon receipt, and simple principal movements. Referencing IRS guidance on virtual currency transactions is essential for correctly characterizing these events. Additionally, if you're addressing "lost" or "stolen" assets, you must meet specific substantiation requirements to claim a loss. Without a clear audit trail, the IRS may disallow these deductions entirely, leaving your blockchain financial records incomplete and your business exposed.

The 2026 Blockchain Financial Record Checklist for US Businesses

Precision is non-negotiable. As the IRS intensifies its focus on digital assets, the burden of proof for every on-chain event rests squarely on your shoulders. Maintaining institutional-grade blockchain financial records requires a shift from passive data collection to active financial stewardship. You must move beyond simple transaction logs to create a comprehensive audit trail that justifies your tax positions. This checklist provides the rigorous framework necessary to ensure your organization remains resilient under federal scrutiny.

- Monthly Wallet Reconciliation: You must verify that your internal ledger balances match the on-chain reality for every custodial and non-custodial wallet.

- Classification of Flows: Every transaction must be tagged with its specific business intent, such as income, expense, or internal transfer, to prevent the IRS from mischaracterizing movements as taxable events.

- Basis Tracking: You need to maintain a chronological history of every asset lot purchased, ensuring your cost basis calculations are accurate for future dispositions.

- Document Association: Every on-chain hash should be linked to a PDF invoice, contract, or receipt to provide the context that raw data lacks.

- Valuation Consistency: Use a single, reputable price oracle for all Fair Market Value (FMV) calculations to ensure your blockchain financial records remain internally consistent.

While custodial brokers will furnish Form 1099-DA by February 15, 2026, for gross proceeds, the responsibility for calculating cost basis remains firmly with the taxpayer for the 2025 tax year. This gap in reporting makes your internal record-keeping even more critical. If you find your current systems are struggling to keep pace with these requirements, you can contact our team to fortify your compliance framework.

Monthly Maintenance Tasks

Perform a "roll-forward" of all wallet balances every 30 days to ensure your records stay synchronized with the blockchain. This process involves identifying the starting balance, adding all inflows, subtracting all outflows, and verifying the result against the ending on-chain balance. You should identify and resolve "unidentified" transactions immediately rather than waiting for year-end. For a deeper dive into this process, read our guide on how to reconcile crypto transactions. Consistent monthly maintenance prevents the accumulation of data debt that leads to audit vulnerabilities.

Year-End Audit Preparation

Your goal is to generate a comprehensive realized gain/loss report for IRS Form 8949 that is beyond reproach. You must also verify that all "airdropped" tokens have been recognized as ordinary income at their fair market value on the date of receipt under IRS rules. We recommend preparing a "Proof of Reserve" report for your internal stakeholders and potential auditors to demonstrate total command over your digital asset holdings. This proactive stance ensures that when an auditor asks for substantiation, you provide a polished narrative rather than a collection of hashes. Our tax filing and reporting services are designed to handle these complexities, ensuring your year-end process is seamless and defensible.

Strategic Oversight: Mastering Digital Asset Reporting with Block3 Finance

Growth requires a foundation of absolute clarity. While the checklists and reconciliation frameworks we've discussed provide a roadmap, executing these tasks at scale requires a partner who understands the nuance of both legacy finance and decentralized protocols. We position ourselves as your Visionary Navigator. Our team doesn't just manage your data; we cultivate it into a high-fidelity narrative that empowers your future growth rather than just defending your past. By transforming raw on-chain activity into institutional-grade blockchain financial records, we ensure you stay ahead of shifting IRS standards with confidence and agency.

We resolve the friction between your digital operations and the rigid expectations of federal auditors. Our methodology integrates every on-ramp and off-ramp event into a unified financial narrative, ensuring that your fiat and crypto holdings are always in sync. This level of oversight turns your compliance burden into a competitive advantage. When your books are clean and your records are defensible, you gain the freedom to innovate without the constant anxiety of a looming IRS examination. We provide the technical rigor and strategic planning necessary to master this volatile landscape.

Expert Crypto Accounting and CFO Services

Scaling a Web3 enterprise demands more than just basic bookkeeping. Our fractional CFO services provide high-level strategic oversight for firms that need sophisticated financial leadership without the cost of a full-time executive. We bring over 13 years of experience in the blockchain ecosystem to every engagement, offering a level of intellectual depth that traditional firms cannot match. Our approach to institutional-grade accounting ensures that your blockchain financial records are not only accurate but also optimized for long-term stability and audit-readiness under IRS rules.

Seamless Compliance Solutions

Navigating the complexities of federal tax law requires a partner who stays ahead of the curve. We specialize in tax filing and reporting for IRS filers, ensuring that every gain, loss, and income event is characterized correctly to minimize your liability. Our expertise extends to on-and-off-ramp compliance, which is essential for businesses operating in a global environment. We handle the heavy lifting of data reconciliation and classification so you can focus on your core mission. It's time to shift from a defensive posture to one of total financial command. Secure your financial future with Block3 Finance and gain the peace of mind that comes with professional, audit-ready oversight.

Secure Your Competitive Advantage in the Digital Asset Economy

The 2026 tax landscape demands more than just basic record-keeping; it requires total financial mastery. You've seen how raw on-chain data fails as a legal defense and why a reconciled general ledger is the only path to safety under IRS rules. By implementing a rigorous monthly checklist and maintaining high-fidelity blockchain financial records, you shift from a position of vulnerability to one of institutional strength. This discipline doesn't just satisfy federal auditors. It provides the strategic clarity you need to scale your operations with absolute confidence.

We've spent over 13 years navigating the complexities of the blockchain ecosystem, earning a top-ranked reputation from Bitcoin.com and serving more than 980 global clients. Our team stands ready to transform your complex smart contract activity into a defensible financial narrative that protects your bottom line. Don't leave your compliance to chance when you can leverage the expertise of a visionary navigator. Master Your On-Chain Records with Block3 Finance and gain the agency to thrive in an evolving market. You've built the future; we'll help you secure it.

Frequently Asked Questions

What specific records does the IRS require for blockchain transactions?

Under IRS rules, you must maintain permanent books that include precise dates, fair market value in USD at the time of the transaction, unique transaction hashes, and all involved wallet addresses. These blockchain financial records must also track the specific cost basis for every asset lot to ensure accurate gain or loss reporting on Form 8949. The burden of proof rests entirely on you to substantiate every inflow and outflow with contemporaneous documentation.

Is a CSV export from my crypto exchange enough for an IRS audit?

A simple CSV export is rarely sufficient for a federal examination because it lacks the necessary on-chain verification and commercial context. These files often fail to distinguish between internal transfers and revenue events, which can lead to double-counting income. You must supplement exchange data with a reconciled general ledger that links each transaction to original source documents, such as digital invoices or vendor contracts, to prove business intent.

How do I determine the fair market value of an illiquid NFT for my records?

To determine the fair market value of an illiquid NFT, you should use the price of comparable assets sold on the same date or a professional appraisal if the value is significant. Under IRS guidance, you must document the specific methodology used for these valuations to ensure your records remain defensible. Maintaining a consistent valuation framework is critical for demonstrating financial rigor and avoiding disputes during an audit.

Does the IRS accept blockchain data as an immutable audit trail?

The IRS recognizes blockchain data as a verifiable audit trail, but they view raw ledger entries as incomplete evidence without supplementary business context. You must provide a reconciled narrative that explains the "why" behind every movement on the public ledger. Without this metadata, agents are legally permitted to characterize unexplained inflows as taxable income by default, shifting the narrative away from your control.

What happens if I cannot find the original purchase price for an old crypto asset?

If you cannot substantiate the original purchase price of an asset, the IRS may assign it a cost basis of zero. This results in the entire proceeds of a future sale being treated as a taxable gain, significantly increasing your tax liability. This is why maintaining proactive blockchain financial records is essential; it preserves your capital by ensuring you only pay tax on your actual economic gains rather than your total proceeds.

How should I record gas fees for failed transactions on the blockchain?

Gas fees for failed transactions are generally treated as deductible business expenses rather than being added to the cost basis of an asset. You should categorize these costs as separate line items in your general ledger to ensure they are properly recognized on your tax return. Recording these failed attempts demonstrates a high level of accounting discipline and ensures you aren't leaving valid deductions on the table due to network friction.

Do I need a separate bank account for my business crypto transactions?

You should maintain a dedicated bank account for your digital asset business to prevent the commingling of personal and professional funds. This separation is vital for maintaining the "corporate veil" and ensuring your financial statements are transparent for federal auditors. A clean break between fiat and crypto operations makes the reconciliation process much smoother and reduces the risk of the IRS piercing your liability protections.

Are blockchain financial records different for DAOs compared to LLCs?

Blockchain financial records for DAOs are governed by how the entity is classified for federal tax purposes, which is often as a partnership or a corporation under IRS rules. While the underlying technology is identical, the reporting requirements for a DAO must align with traditional U.S. business structures to satisfy federal standards. You must ensure that your on-chain governance and treasury movements map correctly to the tax forms required for your specific entity type.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Block3 Finance, with over 26+ years of Canadian and international tax and accounting experience. A crypto accounting specialist since the early days of Bitcoin, he has consulted for over 38 crypto companies and collaborated with legal professionals on regulatory matters. His expertise spans corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, and CRA audits.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Block3 Finance and Tax Partners has 44 full-time accountants and over 9,800+ clients.

Frequently Asked Questions

The Evidence vs. Record Distinction

Defensible blockchain financial records are the synthesis of on-chain data and business intent. Think of the blockchain as the "proof of existence," while your accounting system provides the "proof of characterization." A transaction hash only proves that assets moved from Point A to Point B. It doesn't explain the fair market value at the time of the trade or the tax cost basis of the assets involved. This distinction becomes critical in high-volume environments like DeFi or NFT trading. In these spaces, automated "data noise" can quickly bury meaningful financial activity under thousands of irrelevant smart contract interactions, making manual reconciliation nearly impossible without a structured framework.

IRS Expectations for Digital Asset Documentation

Under IRS rules, specifically Section 6001, every person liable for any tax must keep "permanent books of account or records" that are sufficient to establish the amount of gross income and deductions. The legal burden of proof rests entirely on you, the taxpayer. The IRS increasingly uses sophisticated tools to scrape on-chain data and identify undisclosed income. If your internal documentation doesn't match the public ledger, the discrepancy triggers immediate red flags. You need a robust audit and compliance strategy that transforms anonymous wallet activity into a transparent, GAAP-compliant narrative. This includes maintaining records of: By treating the blockchain as a foundational audit trail rather than a finished product, you gain total command over your financial landscape. This proactive stance shifts you from a defensive position of managing regulations to an offensive one focused on growth and institutional stability. A single transaction hash is a ghost without a body. To transform these digital traces into blockchain financial records that withstand federal scrutiny, you must build a comprehensive data profile for every event. The IRS doesn't just want to see that a transfer occurred; they require proof of the asset's value and the commercial context surrounding it. This means every record must capture the precise timestamp, the fair market value at the moment of receipt, and the associated transaction fees. We believe that mastery over these details is what separates a vulnerable business from one that is truly audit-ready. Gas fees represent a specific point of friction that many firms overlook. Under IRS rules, these network costs are often deductible business expenses or can be added to the cost basis of an acquired asset. By categorizing gas as a separate line item, you reduce your overall tax liability while demonstrating a high level of accounting rigor. We recommend linking every on-chain hash directly to off-chain documentation, such as digital invoices or vendor contracts, to ensure that the business intent is undeniable. If you find this reconciliation process overwhelming, our monthly accounting services can help streamline the data capture and classification.

Metadata Requirements for IRS Compliance

Your internal ledger must track specific fields to satisfy IRS requirements for digital assets. At a minimum, each entry must include the date, the Fair Market Value (FMV) in USD, the unique Transaction ID, and the involved Wallet Addresses. You also have a strict basis tracking requirement for every individual asset in your inventory. Cost basis is the original value of an asset for tax purposes, adjusted for fees. Maintaining this granularity is the only way to accurately calculate gains or losses when you eventually dispose of the asset, especially as the IRS phases in new cost basis reporting requirements for brokers in 2026.

Fair Value Measurement Under ASU 2023-08

The landscape of crypto accounting is shifting toward greater transparency and accuracy. Starting in 2026, ASU 2023-08 requires many U.S. firms to measure their digital assets at fair value on their financial statements. This represents a significant departure from the old historical cost less impairment model, which often resulted in understated balance sheets. This new requirement ensures that your blockchain financial records reflect the actual economic reality of your holdings at the end of each reporting period. While this improves the quality of your financial data, it also demands more frequent and precise valuation methodologies to stay compliant. For those managing more complex portfolios, our CFO services provide the strategic oversight needed to navigate these evolving standards. If you're concerned about how these changes will impact your next filing, it's wise to consult with our team to review your current reporting framework. Triple-entry accounting isn't just a conceptual buzzword; it's the operational reality of any hybrid fiat-crypto business model. While the blockchain provides the third entry as a public proof of transaction, your internal General Ledger (GL) remains the ultimate authority for IRS reporting. The friction arises when you attempt to sync these two worlds. We often see automated sub-ledgers fail to map correctly to QuickBooks or Xero, leading to a fragmented view of your financial health. If your systems don't distinguish between a revenue event and a simple internal transfer between company-owned wallets, you risk double-counting income and inflating your tax liability. This oversight doesn't just cost money; it creates a vulnerability that federal auditors are trained to exploit. A proactive approach to reconciliation is the only way to maintain defensible blockchain financial records. Waiting until year-end to untangle thousands of smart contract interactions is a recipe for disaster. You need a methodical workflow that validates on-chain activity against your bank statements and invoices in real-time. This level of discipline ensures that your books are always ready for scrutiny, shifting you from a defensive posture to one of total command over your financial narrative. We prioritize this continuous verification to resolve discrepancies before they become permanent errors on your tax return.

Bridging the Gap Between Wallets and ERPs

Specialized middleware acts as the vital connective tissue in modern bookkeeping. However, automated data ingestion from exchanges often misses the "why" behind the movement. You might see an inflow but lack the documentation to prove it's a loan repayment rather than sales revenue. This is why manual oversight remains essential. For a deeper look at institutional-grade strategies, explore our guide on digital asset bookkeeping. Relying solely on raw API feeds without human verification often results in misclassified assets and incorrect cost basis tracking, both of which trigger red flags under IRS rules.

Handling Complex On-Chain Events

DeFi activity introduces layers of complexity that traditional accounting software isn't built to handle. Liquidity pool (LP) tokens and wrapped assets require careful tracking of cost basis and fair value to ensure accurate reporting. You must also differentiate between staking rewards, which are generally treated as income upon receipt, and simple principal movements. Referencing IRS guidance on virtual currency transactions is essential for correctly characterizing these events. Additionally, if you're addressing "lost" or "stolen" assets, you must meet specific substantiation requirements to claim a loss. Without a clear audit trail, the IRS may disallow these deductions entirely, leaving your blockchain financial records incomplete and your business exposed. Precision is non-negotiable. As the IRS intensifies its focus on digital assets, the burden of proof for every on-chain event rests squarely on your shoulders. Maintaining institutional-grade blockchain financial records requires a shift from passive data collection to active financial stewardship. You must move beyond simple transaction logs to create a comprehensive audit trail that justifies your tax positions. This checklist provides the rigorous framework necessary to ensure your organization remains resilient under federal scrutiny. While custodial brokers will furnish Form 1099-DA by February 15, 2026, for gross proceeds, the responsibility for calculating cost basis remains firmly with the taxpayer for the 2025 tax year. This gap in reporting makes your internal record-keeping even more critical. If you find your current systems are struggling to keep pace with these requirements, you can contact our team to fortify your compliance framework.

Monthly Maintenance Tasks

Perform a "roll-forward" of all wallet balances every 30 days to ensure your records stay synchronized with the blockchain. This process involves identifying the starting balance, adding all inflows, subtracting all outflows, and verifying the result against the ending on-chain balance. You should identify and resolve "unidentified" transactions immediately rather than waiting for year-end. For a deeper dive into this process, read our guide on how to reconcile crypto transactions. Consistent monthly maintenance prevents the accumulation of data debt that leads to audit vulnerabilities.

Year-End Audit Preparation

Your goal is to generate a comprehensive realized gain/loss report for IRS Form 8949 that is beyond reproach. You must also verify that all "airdropped" tokens have been recognized as ordinary income at their fair market value on the date of receipt under IRS rules. We recommend preparing a "Proof of Reserve" report for your internal stakeholders and potential auditors to demonstrate total command over your digital asset holdings. This proactive stance ensures that when an auditor asks for substantiation, you provide a polished narrative rather than a collection of hashes. Our tax filing and reporting services are designed to handle these complexities, ensuring your year-end process is seamless and defensible. Growth requires a foundation of absolute clarity. While the checklists and reconciliation frameworks we've discussed provide a roadmap, executing these tasks at scale requires a partner who understands the nuance of both legacy finance and decentralized protocols. We position ourselves as your Visionary Navigator. Our team doesn't just manage your data; we cultivate it into a high-fidelity narrative that empowers your future growth rather than just defending your past. By transforming raw on-chain activity into institutional-grade blockchain financial records, we ensure you stay ahead of shifting IRS standards with confidence and agency. We resolve the friction between your digital operations and the rigid expectations of federal auditors. Our methodology integrates every on-ramp and off-ramp event into a unified financial narrative, ensuring that your fiat and crypto holdings are always in sync. This level of oversight turns your compliance burden into a competitive advantage. When your books are clean and your records are defensible, you gain the freedom to innovate without the constant anxiety of a looming IRS examination. We provide the technical rigor and strategic planning necessary to master this volatile landscape.

Expert Crypto Accounting and CFO Services

Scaling a Web3 enterprise demands more than just basic bookkeeping. Our fractional CFO services provide high-level strategic oversight for firms that need sophisticated financial leadership without the cost of a full-time executive. We bring over 13 years of experience in the blockchain ecosystem to every engagement, offering a level of intellectual depth that traditional firms cannot match. Our approach to institutional-grade accounting ensures that your blockchain financial records are not only accurate but also optimized for long-term stability and audit-readiness under IRS rules.

Seamless Compliance Solutions

Navigating the complexities of federal tax law requires a partner who stays ahead of the curve. We specialize in tax filing and reporting for IRS filers, ensuring that every gain, loss, and income event is characterized correctly to minimize your liability. Our expertise extends to on-and-off-ramp compliance, which is essential for businesses operating in a global environment. We handle the heavy lifting of data reconciliation and classification so you can focus on your core mission. It's time to shift from a defensive posture to one of total financial command. Secure your financial future with Block3 Finance and gain the peace of mind that comes with professional, audit-ready oversight. The 2026 tax landscape demands more than just basic record-keeping; it requires total financial mastery. You've seen how raw on-chain data fails as a legal defense and why a reconciled general ledger is the only path to safety under IRS rules. By implementing a rigorous monthly checklist and maintaining high-fidelity blockchain financial records, you shift from a position of vulnerability to one of institutional strength. This discipline doesn't just satisfy federal auditors. It provides the strategic clarity you need to scale your operations with absolute confidence. We've spent over 13 years navigating the complexities of the blockchain ecosystem, earning a top-ranked reputation from Bitcoin.com and serving more than 980 global clients. Our team stands ready to transform your complex smart contract activity into a defensible financial narrative that protects your bottom line. Don't leave your compliance to chance when you can leverage the expertise of a visionary navigator. Master Your On-Chain Records with Block3 Finance and gain the agency to thrive in an evolving market. You've built the future; we'll help you secure it.

What specific records does the IRS require for blockchain transactions?

Under IRS rules, you must maintain permanent books that include precise dates, fair market value in USD at the time of the transaction, unique transaction hashes, and all involved wallet addresses. These blockchain financial records must also track the specific cost basis for every asset lot to ensure accurate gain or loss reporting on Form 8949. The burden of proof rests entirely on you to substantiate every inflow and outflow with contemporaneous documentation.

Is a CSV export from my crypto exchange enough for an IRS audit?

A simple CSV export is rarely sufficient for a federal examination because it lacks the necessary on-chain verification and commercial context. These files often fail to distinguish between internal transfers and revenue events, which can lead to double-counting income. You must supplement exchange data with a reconciled general ledger that links each transaction to original source documents, such as digital invoices or vendor contracts, to prove business intent.

How do I determine the fair market value of an illiquid NFT for my records?

To determine the fair market value of an illiquid NFT, you should use the price of comparable assets sold on the same date or a professional appraisal if the value is significant. Under IRS guidance, you must document the specific methodology used for these valuations to ensure your records remain defensible. Maintaining a consistent valuation framework is critical for demonstrating financial rigor and avoiding disputes during an audit.

Does the IRS accept blockchain data as an immutable audit trail?

The IRS recognizes blockchain data as a verifiable audit trail, but they view raw ledger entries as incomplete evidence without supplementary business context. You must provide a reconciled narrative that explains the "why" behind every movement on the public ledger. Without this metadata, agents are legally permitted to characterize unexplained inflows as taxable income by default, shifting the narrative away from your control.

What happens if I cannot find the original purchase price for an old crypto asset?

If you cannot substantiate the original purchase price of an asset, the IRS may assign it a cost basis of zero. This results in the entire proceeds of a future sale being treated as a taxable gain, significantly increasing your tax liability. This is why maintaining proactive blockchain financial records is essential; it preserves your capital by ensuring you only pay tax on your actual economic gains rather than your total proceeds.

How should I record gas fees for failed transactions on the blockchain?

Gas fees for failed transactions are generally treated as deductible business expenses rather than being added to the cost basis of an asset. You should categorize these costs as separate line items in your general ledger to ensure they are properly recognized on your tax return. Recording these failed attempts demonstrates a high level of accounting discipline and ensures you aren't leaving valid deductions on the table due to network friction.

Do I need a separate bank account for my business crypto transactions?

You should maintain a dedicated bank account for your digital asset business to prevent the commingling of personal and professional funds. This separation is vital for maintaining the "corporate veil" and ensuring your financial statements are transparent for federal auditors. A clean break between fiat and crypto operations makes the reconciliation process much smoother and reduces the risk of the IRS piercing your liability protections.

Are blockchain financial records different for DAOs compared to LLCs?

Blockchain financial records for DAOs are governed by how the entity is classified for federal tax purposes, which is often as a partnership or a corporation under IRS rules. While the underlying technology is identical, the reporting requirements for a DAO must align with traditional U.S. business structures to satisfy federal standards. You must ensure that your on-chain governance and treasury movements map correctly to the tax forms required for your specific entity type.