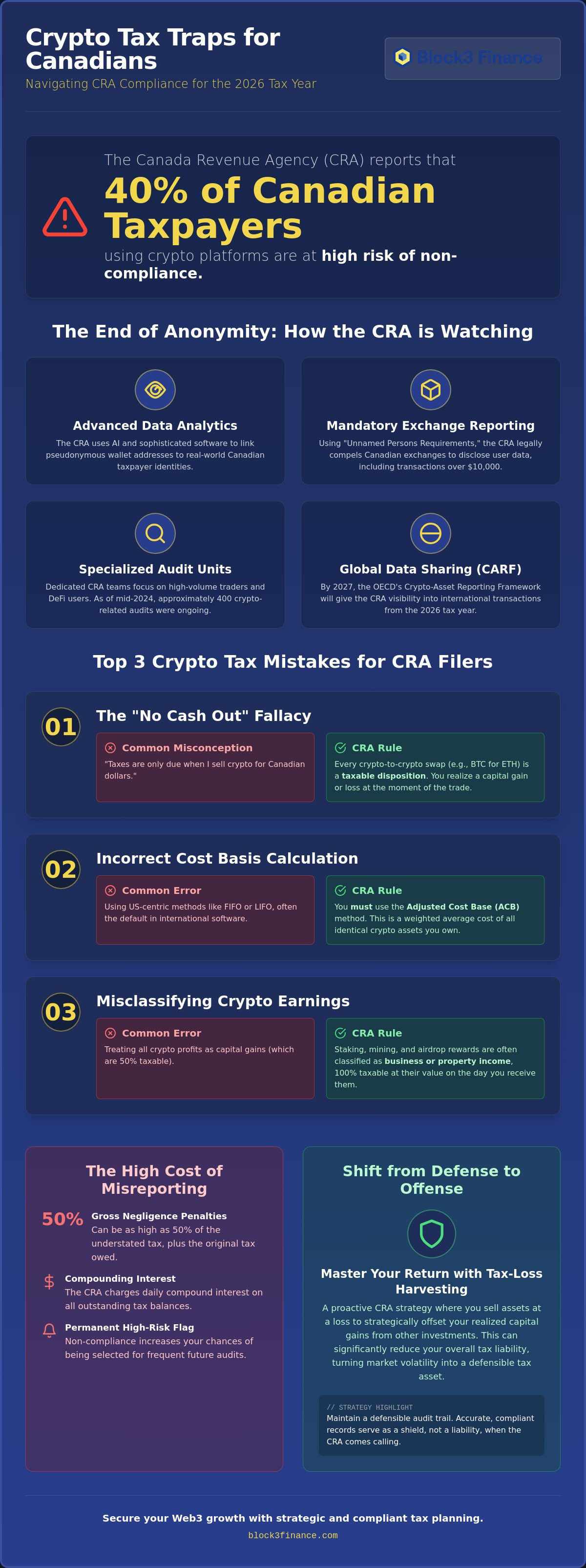

The Canada Revenue Agency reports that 40% of Canadian taxpayers using crypto platforms are at high risk of non-compliance. It's a sobering figure that highlights the friction between rapid digital innovation and the rigid demands of the tax code. You've likely felt the weight of trying to track every DeFi swap or NFT mint; wondering if your Adjusted Cost Base (ACB), which is the weighted average cost of all identical crypto assets you own, will actually hold up under scrutiny. The fear of a CRA audit is legitimate, especially as the agency intensifies its focus on digital assets through AI and enhanced data analytics.

We're here to shift your perspective from defensive management to strategic mastery. By identifying the most common crypto tax mistakes to avoid, you can secure a clean, defensible return and leverage tax-loss harvesting; a strategy where you sell assets at a loss to offset your realized capital gains and reduce your overall tax liability. This guide details seven critical errors that trigger penalties for CRA filers in 2026. It provides the roadmap you need to maintain total command over your financial landscape while protecting your long-term Web3 growth.

Key Takeaways

- Gain clarity on how the CRA utilizes advanced data analytics and mandatory exchange reporting to eliminate anonymity and link digital identities to on-chain activity.

- Identify the most critical crypto tax mistakes to avoid, such as the common misconception that crypto-to-crypto swaps are non-taxable events for Canadian filers.

- Master the Adjusted Cost Base (ACB) method to ensure your cost averaging aligns with CRA requirements; this prevents the audit triggers often caused by utilizing incorrect US-centric calculation models.

- Differentiate between business income and capital gains for staking, mining, and airdrops to accurately report your fiscal obligations at the point of receipt.

- Shift your approach from reactive filing to proactive mastery by implementing tax-loss harvesting strategies that turn market volatility into defensible tax assets.

The Growing Risk of Non-Compliance: Why the CRA is Prioritizing Crypto Audits

The era of perceived anonymity on the blockchain has ended. The CRA now employs sophisticated data analytics to bridge the gap between pseudonymous wallet addresses and real-world identities. This isn't just theory; the CRA has successfully used unnamed persons requirements, which are legal mechanisms that allow the agency to obtain judicial authorization to compel third parties, such as Canadian-based exchanges, to disclose information about unidentified taxpayers. If you've moved more than $10,000 in a single transaction, the CRA likely already has a record of it. This shift in capability marks a transition from "if they find out" to "when they find out" for the 2026 tax year, making it essential to identify the primary crypto tax mistakes to avoid before your return is finalized. Understanding the global legal status of cryptocurrencies helps clarify that Canada's aggressive stance is part of a unified international effort to ensure digital asset transparency.

The CRA’s Digital Asset Strategy in 2026

The CRA has established specialized crypto audit units that focus on high-volume traders and DeFi participants. As of mid-2024, the CRA had approximately 400 ongoing crypto-related audits, a number that continues to grow as their tools evolve. Their objective is clear: identify unreported income from staking, mining, and capital gains, which represent the profit you realize when you sell or swap an asset for a price higher than its original cost. By 2027, the implementation of the OECD’s Crypto-Asset Reporting Framework (CARF) will provide the CRA with even greater visibility into international transactions conducted in 2026. For those who realize they've made errors, the Voluntary Disclosures Program (VDP) offers a pathway to correct filings before an inquiry begins. Engaging in professional CRA crypto audits preparation ensures you have a defensible audit trail before the first letter arrives.

The Consequences of Misreporting in Canada

The CRA distinguishes between "innocent errors" and "gross negligence" under Canadian tax law. While a simple calculation mistake might only result in interest on the unpaid balance, gross negligence penalties can be severe, often reaching 50% of the understated tax. One of the most significant crypto tax mistakes to avoid is the assumption that the CRA won't verify your on-chain history against your bank deposits. The agency's use of blockchain analytics allows them to trace the flow of funds through mixers and bridges, rendering traditional evasion tactics ineffective. Beyond immediate financial penalties, persistent non-compliance can lead to a permanent high-risk flag on your profile, increasing the frequency of future reviews. You should review our guidance on What Happens If I Don’t File Crypto Taxes in Canada? to understand the full scope of risks involving penalties and interest in 2026. We advocate for a proactive stance, where your records serve as a shield rather than a liability.

Mistake #1: Believing Crypto-to-Crypto Swaps are Tax-Free in Canada

Many investors operate under the dangerous delusion that tax liability only triggers when they "cash out" to a traditional bank account. In the eyes of the CRA, this is a fundamental misunderstanding of how digital assets are governed. Every time you swap one token for another, such as trading Bitcoin for Ethereum, you've completed a taxable disposition. One of the most frequent crypto tax mistakes to avoid is the assumption that liability only arises when you exit the market into fiat currency; in reality, the CRA views a crypto-to-crypto trade as two distinct actions: the sale of one asset at its fair market value and the immediate purchase of another.

This "No Cash Out" fallacy often leads to significant, unrecorded tax debts. If you traded a volatile asset at its peak for another token that subsequently crashed, your tax obligation is still based on the value at the moment of the initial trade. This can create a liquidity crisis where you owe more in taxes than your current portfolio is worth. This risk is amplified in decentralized finance (DeFi) environments. When you deposit tokens into a liquidity pool and receive LP tokens in return, or when an automated market maker (AMM) executes a rebalancing trade, you are likely triggering dispositions that must be reported to the CRA.

Calculating Disposition Value in Canadian Dollars

The CRA requires all taxpayers to report their income and capital gains in Canadian dollars (CAD). This means you must determine the Fair Market Value (FMV) of the asset you disposed of at the exact time of the transaction. Under the Income Tax Act as applied to digital assets, a disposition is defined as any transaction where a taxpayer relinquishes control of a property, such as swapping one token for another, which triggers a realization of a gain or loss. While many traders use the "average price of the day," this method is often insufficient for high-volatility assets where prices can swing 20% within hours. You must use a consistent, reputable exchange rate source for all conversions to maintain a defensible audit trail.

Stablecoin Swaps: The Hidden Tax Trigger

Swapping a volatile asset for a stablecoin like USDT or USDC is a common strategy to preserve capital, but it doesn't pause your tax obligations. These trades are still dispositions under CRA rules. Furthermore, you must account for the fluctuations in the CAD/USD exchange rate; even if the stablecoin stays at $1.00 USD, its value in Canadian dollars changes daily. Managing these high-frequency data points requires precision, which is why professional accounting services are vital for active traders. If you are unsure how your 2026 trades impact your liability, you should consult with our strategists to ensure your reporting is accurate and optimized.

The Adjusted Cost Base (ACB) Nightmare: Why Averaging Errors Lead to Audits

Calculating your tax liability in Canada requires more than just subtracting your purchase price from your sale price. The CRA mandates the use of the Adjusted Cost Base (ACB) method for all identical properties. This means you must track the weighted average cost of every unit of a specific cryptocurrency you own, regardless of where it is stored. One of the most pervasive crypto tax mistakes to avoid is adopting US-centric calculation methods like First-In, First-Out (FIFO) or Last-In, First-Out (LIFO). While these methods are common in American tax software, they are generally not permitted for personal filers under CRA regulations; using them can result in significant discrepancies that trigger an audit.

The complexity scales with every wallet, exchange, and cold storage device you add to your ecosystem. The CRA views your entire holdings of a single asset as one "pool." If you buy Bitcoin on three different exchanges, you don't have three separate cost bases; you have one consolidated ACB. This single-pool requirement often leads to errors when traders fail to account for transfer fees or fail to sync all their transaction data into a single source of truth. Mastering this data isn't just about compliance; it's about gaining total command over your financial trajectory and ensuring your records are beyond reproach.

Identical Property Rules for Canadians

Under CRA guidelines, an identical property is any asset that is the same in all material respects, such as two units of the same cryptocurrency. To calculate your ACB, you add the cost of new purchases to the existing cost base and divide by the total number of units held. This weighted average must be updated every time you acquire more of the asset. For CRA filers, the superficial loss rule dictates that a capital loss is disallowed if you purchase the same or identical property within 30 days before or after the sale and still own it at the end of that period.

Software vs. Specialized Accountants for ACB

Generic tax software often struggles with the specific nuances of Canadian tax law, particularly regarding complex DeFi transactions and the superficial loss rule. These automated tools frequently miss the subtle details required to build a defensible return. Our team at Block3 Finance bridges this gap by providing human expertise that software alone cannot replicate. You can explore the differences in our guide on Crypto Accounting Software vs. Accountant for Canadian Filers. By maintaining audit-ready books, we transform your accounting from a year-end scramble into a strategic asset that protects your long-term wealth.

The "Income vs. Capital Gains" Trap: Misclassifying Staking, Mining, and Airdrops

One of the most consequential crypto tax mistakes to avoid is the misclassification of how you acquire digital assets. For CRA filers, the distinction between capital gains and business income isn't a choice; it's a legal determination based on the nature of your activity. Staking rewards and mining income are generally treated as business income. This means the fair market value of the token at the time of receipt is 100% taxable as income. When you eventually sell those tokens, any further increase in value is treated as a capital gain, using that initial fair market value as your cost basis. Misreporting these as capital gains from the start can lead to significant back-taxes and interest if the CRA reclassifies your activity during an audit.

Airdrops and hard forks present another layer of complexity. While some investors assume these tokens have no tax impact until they're sold, the CRA typically views them as taxable income at their fair market value on the date they are received. Tracking this initial value correctly is essential for your records. If you fail to record the value at receipt, you'll struggle to calculate an accurate Adjusted Cost Base (ACB) later, which often leads to overpaying on future capital gains or triggering an audit for unreported income. Your goal is to move from a defensive posture of "hoping for the best" to a proactive mastery of your on-chain history.

When Does Investing Become a Business?

The CRA analyzes several factors to determine if your crypto activity constitutes a business. They look at transaction frequency, the level of specialized knowledge you apply, and whether your primary intent is to generate short-term profit through active trading. If your activity mirrors a commercial enterprise, your gains are taxed at 100% inclusion. For those classified as investors, the 2026 capital gains inclusion rate is 50% on the first $250,000 of gains, rising to 66.67% for amounts exceeding that threshold. Web3 startups and high-volume traders require specialized CFO services to navigate these structural nuances and ensure their tax strategy supports long-term growth.

DeFi Yield and Liquidity Provision

In the DeFi space, even simple technical movements can trigger tax obligations. Swapping ETH for "wrapped" versions like wETH is considered a disposition under CRA rules, even if the value is pegged 1:1. Gas fees incurred during these trades should generally be added to your Adjusted Cost Base (ACB) of the acquired asset rather than being treated as a separate deductible expense for personal filers. Returns from lending protocols or liquidity pools are typically treated as interest-like income, requiring precise, real-time tracking to avoid year-end discrepancies. To ensure your 2026 filing correctly distinguishes between your investment and business activities, book a consultation with our tax strategists today.

Moving from Defense to Offense: Strategic Tax Planning with Block3 Finance

Transitioning from basic compliance to sophisticated strategy marks the difference between a reactive taxpayer and a master of their digital wealth. While identifying the primary crypto tax mistakes to avoid is the first step toward security, true financial agency requires a proactive approach that anticipates market movements and regulatory shifts. For high-net-worth investors and crypto-native enterprises in Canada, this often involves complex corporate structuring to manage the 2026 inclusion rates, which sit at 66.67% for capital gains exceeding $250,000. By integrating seamless on- and off-ramp solutions, you maintain the clear, immutable financial records required to defend your position before the CRA ever initiates an inquiry.

Strategic mastery also means understanding the impact of federal tax brackets on your total liability. With the top federal rate reaching 33% for income over $258,482 in 2026, every misclassification of business income versus capital gains becomes a costly error. We help you shift the narrative from merely managing regulations to an offensive posture focused on growth and intellectual leadership. This disciplined approach ensures that your vision and execution are inseparable, allowing you to navigate the volatile Web3 landscape with total command.

Tax-Loss Harvesting for Canadians

Tax-loss harvesting is one of the most powerful tools in a Canadian investor's arsenal. It allows you to strategically sell assets that have declined in value to offset capital gains realized earlier in the year. However, you must carefully navigate the CRA's superficial loss rule, which invalidates a loss claim if you buy the same asset within 30 days. Relying on an annual scramble in April often means missing these critical windows for optimization. Establishing a year-round accounting relationship ensures you can execute these maneuvers with precision, turning market volatility into a strategic tax asset.

The Block3 Advantage: 13 Years of Blockchain Expertise

Block3 Finance brings 13 years of deep blockchain immersion to the table. We don't just record transactions; we serve as a Visionary Navigator, translating complex on-chain data into clean, defensible records. Our expertise in specialized tax filing and reporting provides global Web3 entities with the stability needed to thrive in a volatile industry. We move beyond the dry nature of traditional accounting to offer a roadmap for growth and total command over your financial landscape. Secure your financial future with a professional crypto tax strategy and turn your compliance obligations into a competitive advantage.

Secure Your Digital Legacy in the 2026 Tax Landscape

The path to long-term digital asset growth is paved with meticulous compliance and strategic foresight. You've learned that every swap constitutes a taxable disposition and that the CRA's single-pool requirement for Adjusted Cost Base (ACB) calculations leaves no room for error. By fortifying your reporting against these common crypto tax mistakes to avoid, you transition from a defensive posture to one of total command over your financial trajectory. Precise classification of staking rewards and proactive tracking of airdrops are no longer optional; they're the pillars of a defensible audit trail.

Block3 Finance stands as a calm force in this volatile industry. Top-ranked by Bitcoin.com and backed by 13+ years of blockchain financial expertise, we've empowered over 980 global clients to navigate high-stakes regulatory environments with confidence. We don't just manage your filings; we cultivate a roadmap for your continued evolution in the Web3 space. Our team turns complex on-chain data into a strategic asset that protects your wealth against shifting CRA mandates.

Take the next step in your financial journey. Master your crypto compliance with Block3 Finance’s expert tax services. You possess the vision to innovate; we provide the technical rigor to ensure your success remains uninterrupted.

Frequently Asked Questions

Do I have to pay taxes on crypto if I didn’t sell it for Canadian Dollars?

Yes, you must pay taxes on cryptocurrency even if you haven't converted it to Canadian Dollars. The CRA treats swapping one digital asset for another or using crypto to purchase goods as a barter transaction. These events trigger a disposition, which requires you to calculate the fair market value in CAD at the time of the trade to determine your gain or loss.

How does the CRA track my cryptocurrency transactions?

The CRA monitors digital asset activity through blockchain analytics and mandatory reporting from Canadian-based exchanges. They've successfully used "unnamed persons" requirements to access user records from major platforms. International agreements like the Crypto-Asset Reporting Framework (CARF) will also provide the agency with visibility into foreign exchange activity conducted by Canadian residents.

What is the difference between capital gains and income for crypto in Canada?

The primary difference lies in the inclusion rate applied to your profits. Capital gains generally apply to long-term investors and have a 50% inclusion rate on the first $250,000, whereas business income is 100% taxable. The CRA determines your status based on trading frequency, your level of specialized knowledge, and whether your primary intent is short-term profit.

Can I claim a tax deduction for lost or stolen cryptocurrency?

You can claim a capital loss for lost or stolen cryptocurrency, but you must provide substantial evidence to the CRA. This proof often includes police reports, transaction IDs showing the theft, or technical evidence that a private key is permanently inaccessible. Because the CRA scrutinizes these claims heavily, avoiding documentation gaps is one of the most vital crypto tax mistakes to avoid.

What is the "Superficial Loss" rule and how does it affect my crypto taxes?

The superficial loss rule prevents you from claiming a capital loss if you buy the same or identical cryptocurrency within 30 days before or after the sale. If you still own that asset at the end of the 30-day window, the CRA disallows the loss and adds it to the cost base of the new units. This rule effectively stops wash trading intended solely to reduce tax liability.

Is swapping one cryptocurrency for another a taxable event in Canada?

Yes, every crypto-to-crypto swap is a taxable event under CRA guidelines. The agency views these trades as a simultaneous disposition of one asset and acquisition of another. You're required to record the fair market value in Canadian dollars at the moment the trade occurs to ensure your capital gains or business income is reported accurately.

How long do I need to keep my crypto transaction records for the CRA?

You must keep all cryptocurrency transaction records for at least six years from the end of the tax year they relate to. These records should include transaction dates, wallet addresses, exchange statements, and CAD fair market values. Having a clean, six-year audit trail is a hallmark of a proactive and defensible tax strategy.

What happens if I make a mistake on a previous year’s crypto tax return?

If you find an error on a past return, you can file a T1 Adjustment Request or use the Voluntary Disclosures Program (VDP). Proactively correcting mistakes before the CRA initiates an audit can significantly reduce or eliminate potential penalties. Taking an offensive posture by fixing errors early protects your long-term wealth and maintains your standing with the agency.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Block3 Finance, with over 26+ years of Canadian and international tax and accounting experience. A crypto accounting specialist since the early days of Bitcoin, he has consulted for over 38 crypto companies and collaborated with legal professionals on regulatory matters. His expertise spans corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, and CRA audits.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Block3 Finance and Tax Partners has 44 full-time accountants and over 9,800+ clients.

Frequently Asked Questions

The CRA’s Digital Asset Strategy in 2026

The CRA has established specialized crypto audit units that focus on high-volume traders and DeFi participants. As of mid-2024, the CRA had approximately 400 ongoing crypto-related audits, a number that continues to grow as their tools evolve. Their objective is clear: identify unreported income from staking, mining, and capital gains, which represent the profit you realize when you sell or swap an asset for a price higher than its original cost. By 2027, the implementation of the OECD’s Crypto-Asset Reporting Framework (CARF) will provide the CRA with even greater visibility into international transactions conducted in 2026. For those who realize they've made errors, the Voluntary Disclosures Program (VDP) offers a pathway to correct filings before an inquiry begins. Engaging in professional CRA crypto audits preparation ensures you have a defensible audit trail before the first letter arrives.

The Consequences of Misreporting in Canada

The CRA distinguishes between "innocent errors" and "gross negligence" under Canadian tax law. While a simple calculation mistake might only result in interest on the unpaid balance, gross negligence penalties can be severe, often reaching 50% of the understated tax. One of the most significant crypto tax mistakes to avoid is the assumption that the CRA won't verify your on-chain history against your bank deposits. The agency's use of blockchain analytics allows them to trace the flow of funds through mixers and bridges, rendering traditional evasion tactics ineffective. Beyond immediate financial penalties, persistent non-compliance can lead to a permanent high-risk flag on your profile, increasing the frequency of future reviews. You should review our guidance on What Happens If I Don’t File Crypto Taxes in Canada? to understand the full scope of risks involving penalties and interest in 2026. We advocate for a proactive stance, where your records serve as a shield rather than a liability. Many investors operate under the dangerous delusion that tax liability only triggers when they "cash out" to a traditional bank account. In the eyes of the CRA, this is a fundamental misunderstanding of how digital assets are governed. Every time you swap one token for another, such as trading Bitcoin for Ethereum, you've completed a taxable disposition. One of the most frequent crypto tax mistakes to avoid is the assumption that liability only arises when you exit the market into fiat currency; in reality, the CRA views a crypto-to-crypto trade as two distinct actions: the sale of one asset at its fair market value and the immediate purchase of another. This "No Cash Out" fallacy often leads to significant, unrecorded tax debts. If you traded a volatile asset at its peak for another token that subsequently crashed, your tax obligation is still based on the value at the moment of the initial trade. This can create a liquidity crisis where you owe more in taxes than your current portfolio is worth. This risk is amplified in decentralized finance (DeFi) environments. When you deposit tokens into a liquidity pool and receive LP tokens in return, or when an automated market maker (AMM) executes a rebalancing trade, you are likely triggering dispositions that must be reported to the CRA.

Calculating Disposition Value in Canadian Dollars

The CRA requires all taxpayers to report their income and capital gains in Canadian dollars (CAD). This means you must determine the Fair Market Value (FMV) of the asset you disposed of at the exact time of the transaction. Under the Income Tax Act as applied to digital assets, a disposition is defined as any transaction where a taxpayer relinquishes control of a property, such as swapping one token for another, which triggers a realization of a gain or loss. While many traders use the "average price of the day," this method is often insufficient for high-volatility assets where prices can swing 20% within hours. You must use a consistent, reputable exchange rate source for all conversions to maintain a defensible audit trail.

Stablecoin Swaps: The Hidden Tax Trigger

Swapping a volatile asset for a stablecoin like USDT or USDC is a common strategy to preserve capital, but it doesn't pause your tax obligations. These trades are still dispositions under CRA rules. Furthermore, you must account for the fluctuations in the CAD/USD exchange rate; even if the stablecoin stays at $1.00 USD, its value in Canadian dollars changes daily. Managing these high-frequency data points requires precision, which is why professional accounting services are vital for active traders. If you are unsure how your 2026 trades impact your liability, you should consult with our strategists to ensure your reporting is accurate and optimized. Calculating your tax liability in Canada requires more than just subtracting your purchase price from your sale price. The CRA mandates the use of the Adjusted Cost Base (ACB) method for all identical properties. This means you must track the weighted average cost of every unit of a specific cryptocurrency you own, regardless of where it is stored. One of the most pervasive crypto tax mistakes to avoid is adopting US-centric calculation methods like First-In, First-Out (FIFO) or Last-In, First-Out (LIFO). While these methods are common in American tax software, they are generally not permitted for personal filers under CRA regulations; using them can result in significant discrepancies that trigger an audit. The complexity scales with every wallet, exchange, and cold storage device you add to your ecosystem. The CRA views your entire holdings of a single asset as one "pool." If you buy Bitcoin on three different exchanges, you don't have three separate cost bases; you have one consolidated ACB. This single-pool requirement often leads to errors when traders fail to account for transfer fees or fail to sync all their transaction data into a single source of truth. Mastering this data isn't just about compliance; it's about gaining total command over your financial trajectory and ensuring your records are beyond reproach.

Identical Property Rules for Canadians

Under CRA guidelines, an identical property is any asset that is the same in all material respects, such as two units of the same cryptocurrency. To calculate your ACB, you add the cost of new purchases to the existing cost base and divide by the total number of units held. This weighted average must be updated every time you acquire more of the asset. For CRA filers, the superficial loss rule dictates that a capital loss is disallowed if you purchase the same or identical property within 30 days before or after the sale and still own it at the end of that period.

Software vs. Specialized Accountants for ACB

Generic tax software often struggles with the specific nuances of Canadian tax law, particularly regarding complex DeFi transactions and the superficial loss rule. These automated tools frequently miss the subtle details required to build a defensible return. Our team at Block3 Finance bridges this gap by providing human expertise that software alone cannot replicate. You can explore the differences in our guide on Crypto Accounting Software vs. Accountant for Canadian Filers. By maintaining audit-ready books, we transform your accounting from a year-end scramble into a strategic asset that protects your long-term wealth. One of the most consequential crypto tax mistakes to avoid is the misclassification of how you acquire digital assets. For CRA filers, the distinction between capital gains and business income isn't a choice; it's a legal determination based on the nature of your activity. Staking rewards and mining income are generally treated as business income. This means the fair market value of the token at the time of receipt is 100% taxable as income. When you eventually sell those tokens, any further increase in value is treated as a capital gain, using that initial fair market value as your cost basis. Misreporting these as capital gains from the start can lead to significant back-taxes and interest if the CRA reclassifies your activity during an audit. Airdrops and hard forks present another layer of complexity. While some investors assume these tokens have no tax impact until they're sold, the CRA typically views them as taxable income at their fair market value on the date they are received. Tracking this initial value correctly is essential for your records. If you fail to record the value at receipt, you'll struggle to calculate an accurate Adjusted Cost Base (ACB) later, which often leads to overpaying on future capital gains or triggering an audit for unreported income. Your goal is to move from a defensive posture of "hoping for the best" to a proactive mastery of your on-chain history.

When Does Investing Become a Business?

The CRA analyzes several factors to determine if your crypto activity constitutes a business. They look at transaction frequency, the level of specialized knowledge you apply, and whether your primary intent is to generate short-term profit through active trading. If your activity mirrors a commercial enterprise, your gains are taxed at 100% inclusion. For those classified as investors, the 2026 capital gains inclusion rate is 50% on the first $250,000 of gains, rising to 66.67% for amounts exceeding that threshold. Web3 startups and high-volume traders require specialized CFO services to navigate these structural nuances and ensure their tax strategy supports long-term growth.

DeFi Yield and Liquidity Provision

In the DeFi space, even simple technical movements can trigger tax obligations. Swapping ETH for "wrapped" versions like wETH is considered a disposition under CRA rules, even if the value is pegged 1:1. Gas fees incurred during these trades should generally be added to your Adjusted Cost Base (ACB) of the acquired asset rather than being treated as a separate deductible expense for personal filers. Returns from lending protocols or liquidity pools are typically treated as interest-like income, requiring precise, real-time tracking to avoid year-end discrepancies. To ensure your 2026 filing correctly distinguishes between your investment and business activities, book a consultation with our tax strategists today. Transitioning from basic compliance to sophisticated strategy marks the difference between a reactive taxpayer and a master of their digital wealth. While identifying the primary crypto tax mistakes to avoid is the first step toward security, true financial agency requires a proactive approach that anticipates market movements and regulatory shifts. For high-net-worth investors and crypto-native enterprises in Canada, this often involves complex corporate structuring to manage the 2026 inclusion rates, which sit at 66.67% for capital gains exceeding $250,000. By integrating seamless on- and off-ramp solutions, you maintain the clear, immutable financial records required to defend your position before the CRA ever initiates an inquiry. Strategic mastery also means understanding the impact of federal tax brackets on your total liability. With the top federal rate reaching 33% for income over $258,482 in 2026, every misclassification of business income versus capital gains becomes a costly error. We help you shift the narrative from merely managing regulations to an offensive posture focused on growth and intellectual leadership. This disciplined approach ensures that your vision and execution are inseparable, allowing you to navigate the volatile Web3 landscape with total command.

Tax-Loss Harvesting for Canadians

Tax-loss harvesting is one of the most powerful tools in a Canadian investor's arsenal. It allows you to strategically sell assets that have declined in value to offset capital gains realized earlier in the year. However, you must carefully navigate the CRA's superficial loss rule, which invalidates a loss claim if you buy the same asset within 30 days. Relying on an annual scramble in April often means missing these critical windows for optimization. Establishing a year-round accounting relationship ensures you can execute these maneuvers with precision, turning market volatility into a strategic tax asset.

The Block3 Advantage: 13 Years of Blockchain Expertise

Block3 Finance brings 13 years of deep blockchain immersion to the table. We don't just record transactions; we serve as a Visionary Navigator, translating complex on-chain data into clean, defensible records. Our expertise in specialized tax filing and reporting provides global Web3 entities with the stability needed to thrive in a volatile industry. We move beyond the dry nature of traditional accounting to offer a roadmap for growth and total command over your financial landscape. Secure your financial future with a professional crypto tax strategy and turn your compliance obligations into a competitive advantage. The path to long-term digital asset growth is paved with meticulous compliance and strategic foresight. You've learned that every swap constitutes a taxable disposition and that the CRA's single-pool requirement for Adjusted Cost Base (ACB) calculations leaves no room for error. By fortifying your reporting against these common crypto tax mistakes to avoid, you transition from a defensive posture to one of total command over your financial trajectory. Precise classification of staking rewards and proactive tracking of airdrops are no longer optional; they're the pillars of a defensible audit trail. Block3 Finance stands as a calm force in this volatile industry. Top-ranked by Bitcoin.com and backed by 13+ years of blockchain financial expertise, we've empowered over 980 global clients to navigate high-stakes regulatory environments with confidence. We don't just manage your filings; we cultivate a roadmap for your continued evolution in the Web3 space. Our team turns complex on-chain data into a strategic asset that protects your wealth against shifting CRA mandates. Take the next step in your financial journey. Master your crypto compliance with Block3 Finance’s expert tax services. You possess the vision to innovate; we provide the technical rigor to ensure your success remains uninterrupted.

Do I have to pay taxes on crypto if I didn’t sell it for Canadian Dollars?

Yes, you must pay taxes on cryptocurrency even if you haven't converted it to Canadian Dollars. The CRA treats swapping one digital asset for another or using crypto to purchase goods as a barter transaction. These events trigger a disposition, which requires you to calculate the fair market value in CAD at the time of the trade to determine your gain or loss.

How does the CRA track my cryptocurrency transactions?

The CRA monitors digital asset activity through blockchain analytics and mandatory reporting from Canadian-based exchanges. They've successfully used "unnamed persons" requirements to access user records from major platforms. International agreements like the Crypto-Asset Reporting Framework (CARF) will also provide the agency with visibility into foreign exchange activity conducted by Canadian residents.

What is the difference between capital gains and income for crypto in Canada?

The primary difference lies in the inclusion rate applied to your profits. Capital gains generally apply to long-term investors and have a 50% inclusion rate on the first $250,000, whereas business income is 100% taxable. The CRA determines your status based on trading frequency, your level of specialized knowledge, and whether your primary intent is short-term profit.

Can I claim a tax deduction for lost or stolen cryptocurrency?

You can claim a capital loss for lost or stolen cryptocurrency, but you must provide substantial evidence to the CRA. This proof often includes police reports, transaction IDs showing the theft, or technical evidence that a private key is permanently inaccessible. Because the CRA scrutinizes these claims heavily, avoiding documentation gaps is one of the most vital crypto tax mistakes to avoid.

What is the "Superficial Loss" rule and how does it affect my crypto taxes?

The superficial loss rule prevents you from claiming a capital loss if you buy the same or identical cryptocurrency within 30 days before or after the sale. If you still own that asset at the end of the 30-day window, the CRA disallows the loss and adds it to the cost base of the new units. This rule effectively stops wash trading intended solely to reduce tax liability.

Is swapping one cryptocurrency for another a taxable event in Canada?

Yes, every crypto-to-crypto swap is a taxable event under CRA guidelines. The agency views these trades as a simultaneous disposition of one asset and acquisition of another. You're required to record the fair market value in Canadian dollars at the moment the trade occurs to ensure your capital gains or business income is reported accurately.

How long do I need to keep my crypto transaction records for the CRA?

You must keep all cryptocurrency transaction records for at least six years from the end of the tax year they relate to. These records should include transaction dates, wallet addresses, exchange statements, and CAD fair market values. Having a clean, six-year audit trail is a hallmark of a proactive and defensible tax strategy.

What happens if I make a mistake on a previous year’s crypto tax return?

If you find an error on a past return, you can file a T1 Adjustment Request or use the Voluntary Disclosures Program (VDP). Proactively correcting mistakes before the CRA initiates an audit can significantly reduce or eliminate potential penalties. Taking an offensive posture by fixing errors early protects your long-term wealth and maintains your standing with the agency.