")

Choosing the most obvious legal entity for your startup might actually be your most expensive mistake. While many founders view corporate formation as a simple box-ticking exercise, crypto business incorporation canada requires a sophisticated strategy that balances legal protection with the reality of on-chain transparency. You're likely already feeling the pressure of building an audit trail that satisfies the CRA while avoiding the trap of double taxation on your fiat ramps.

We understand that the volatility of the blockchain space shouldn't extend to your tax liability. This guide provides a definitive framework for selecting an entity that ensures you're protected, compliant, and ready for growth. You'll master the complexities of the 2026 capital gains inclusion rates and the new Crypto-Asset Reporting Framework (CARF) requirements. We'll explore how the right structure reduces your tax burden under the Income Tax Act and transforms chaotic transaction data into a defensible, audit-ready financial record.

Key Takeaways

- Selecting the optimal entity structure allows Canadian founders to leverage small business deductions, potentially reducing the federal tax rate to 9% on the first $500,000 of active business income.

- Strategic crypto business incorporation canada provides the necessary financial architecture to transform complex on-chain activity into a transparent, defensible audit trail.

- Establishing clear corporate boundaries through proper entity selection eliminates the risk of asset commingling, ensuring your venture remains compliant with 2026 CRA reporting standards.

- Mastering cross-border compliance is essential for navigating Foreign Accrual Property Income (FAPI) traps and leveraging tax treaties to protect your global revenue from double taxation.

- Integrating professional on and off-ramp solutions directly into your corporate framework creates a seamless flow between digital assets and fiat, facilitating high-level CFO oversight.

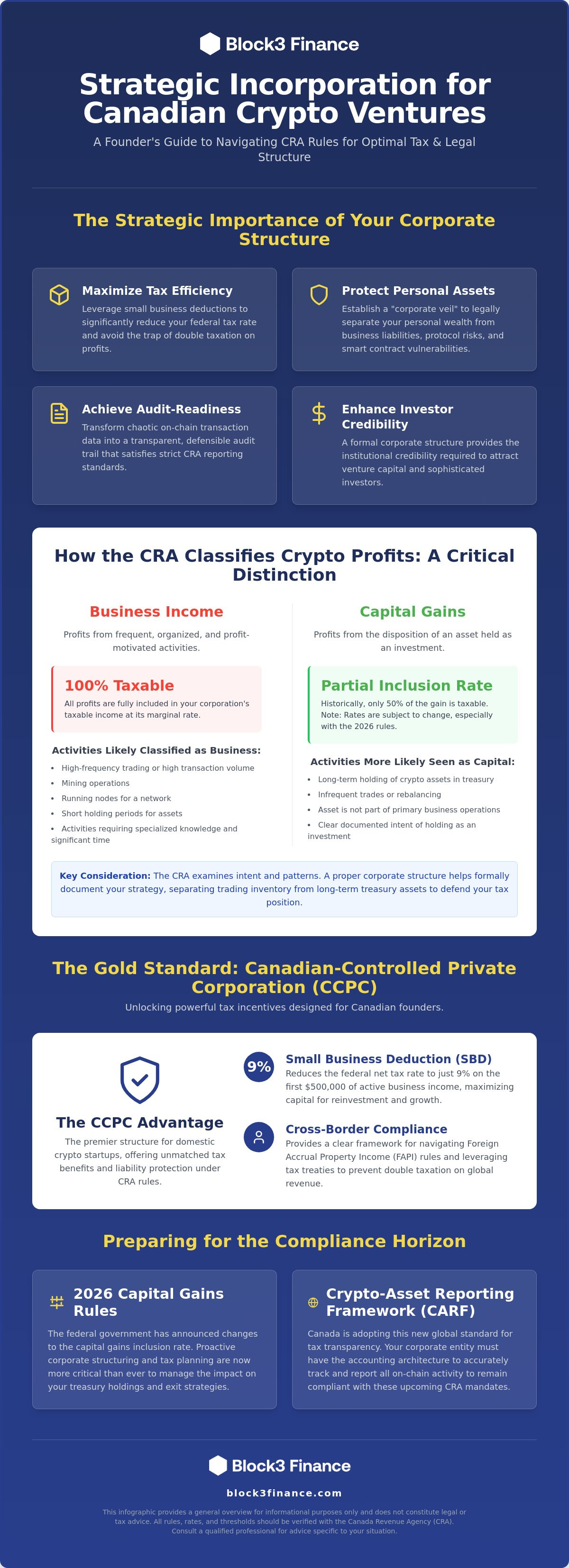

The Strategic Importance of Entity Selection under CRA Rules

Corporate structuring serves as the North Star for your venture's financial health. It dictates every future interaction with the Canada Revenue Agency (CRA) and determines whether your profits are shielded or exposed. In the context of crypto business incorporation canada, the entity you select isn't merely a legal shell; it's a strategic tool designed to manage the complexities of the Canadian Income Tax Act. Under CRA rules, the distinction between a hobbyist and a professional operation rests entirely on the intent and execution of your activities.

The legal status of cryptocurrencies in Canada treats digital assets as a commodity rather than legal tender. This classification means every trade, swap, or sale triggers a specific tax event. Without a formal corporate structure, you risk having 100% of your gains taxed as business income at high personal marginal rates. A deliberate formation strategy ensures you aren't just reacting to tax season but proactively cultivating a sustainable tax profile.

Defining Business Income vs. Capital Gains for Corporations

The CRA applies specific tests to determine if your crypto activity constitutes a business. They look closely at the frequency of your transactions, the period of ownership, and your level of specialized knowledge. If you're running a node, mining, or executing high-frequency trades, the CRA will likely classify your profits as 100% taxable business income. The CRA examines several factors to decide if you're operating a business:

- Transaction volume and frequency of trades.

- The length of time assets are held in your wallets.

- Your expertise and the time spent on crypto activities.

- Whether the activity is clearly for profit or a personal endeavor.

For corporations, the scrutiny is even more intense. Unlike individual filers who might claim the 50% capital gains inclusion rate on the first $250,000 under 2026 rules, a corporation's primary purpose is often presumed to be profit-generating. Establishing your entity with clear, documented intentions is vital. Failure to distinguish between long-term treasury holdings and active trading capital can lead to devastating reassessments and unexpected tax liabilities that stall your growth.

Liability Protection and the Corporate Veil in Web3

Operating in the decentralized space introduces unique protocol risks and smart contract vulnerabilities. A formal crypto business incorporation canada creates a robust corporate veil, which is a legal boundary that separates your personal wealth from the inherent volatility of the blockchain. This protection is essential when engaging with DeFi protocols or managing liquidity pools where technical failures can occur without warning.

Beyond protection, a formal structure provides the institutional credibility required to attract venture capital and sophisticated investors. Using corporate resolutions to document treasury decisions, such as shifting assets into stablecoins or participating in governance, creates a transparent paper trail. This level of corporate structuring ensures that when the CRA or an investor looks at your books, they see a disciplined organization rather than a disorganized collection of wallets.

Comparing Canadian Corporate Structures for Digital Asset Operations

Selecting a legal framework for your digital asset venture requires more than just filing paperwork. It's a strategic decision that determines your access to significant tax incentives. While generic online advice often promotes the flexibility of American-style LLCs, those structures are treated very differently in Canada. For founders pursuing crypto business incorporation canada, the choice usually centers on the Canadian-Controlled Private Corporation (CCPC) versus a general corporate structure.

The CCPC Advantage: Small Business Deductions and Tax Credits

The CCPC remains the gold standard for domestic startups. Under CRA rules, a CCPC can access the Small Business Deduction (SBD), which reduces the federal net tax rate to just 9% on the first $500,000 of active business income. When combined with provincial rates, which range from 0% to 3.2% for small businesses in 2026, this creates a powerful environment for reinvesting profits into your protocol or platform. The CRA's guide for cryptocurrency users emphasizes that business income is fully taxable, making these deductions essential for cash flow management.

Beyond the SBD, CCPCs are eligible for the Scientific Research and Experimental Development (SR&ED) tax incentive. If your team is developing novel blockchain protocols or solving complex consensus challenges, you could recover a significant portion of your R&D expenditures through refundable tax credits. This isn't just about saving money; it's about leveraging government-backed capital to accelerate your technical roadmap and maintain a competitive edge in the global Web3 ecosystem.

Holding Companies (Holdcos) for Treasury Management

As your venture scales, protecting your on-chain assets from operational liabilities becomes paramount. A Holding Company (Holdco) acts as a secure vault for your long-term crypto treasury. By moving profits from your Operating Company (Opco) to your Holdco through inter-corporate dividends, you can often transfer funds without immediate tax consequences. This structure allows you to separate your high-risk daily operations, such as exchange integrations or smart contract deployments, from your core wealth.

- Risk Mitigation: Isolate protocol risks and potential operational lawsuits from your primary asset base.

- Tax Efficiency: Reinvest inter-corporate dividends into new digital asset classes or traditional investments under a protected umbrella.

- Strategic Ramping: Use your Holdco to manage on and off-ramp activity, creating a clear distinction between operational expenses and long-term investments.

If your project involves non-resident directors or significant foreign investment, a General Corporation (Non-CCPC) might be necessary. While you'll lose the 9% small business rate and pay the 15% federal general rate, you gain the ability to structure global partnerships. If you're unsure which path aligns with your five-year vision, consulting with a specialist strategist can help clarify the nuances of the Income Tax Act for your specific use case.

Why Your Structure Dictates Your Accounting and Audit-Readiness

The blueprint you choose for your crypto business incorporation canada directly determines the friction you'll encounter during every month-end close. Many founders prioritize legal registration but overlook the accounting architecture required to maintain a defensible ledger. If your wallet structure doesn't mirror your corporate nodes, you're creating a reconciliation nightmare that invites CRA scrutiny. A well-designed structure isn't just a tax shield; it's the foundation of a clean financial history, and for insights into building a professional fiscal framework in 2026, you can visit Cairns Quality Accounting to learn more about smarter business finances.

Commingling personal and business assets is the fastest way to lose the protection of the corporate veil. The CRA demands clear boundaries. They expect to see that your corporate entity owns the private keys and that all on-chain activity serves a documented business purpose. Proper structuring allows you to align your wallet architecture with your legal framework, ensuring that blockchain financial records are transparent and verifiable from the moment of inception. This alignment reduces the time spent on manual reconciliations and provides a clear path for future growth.

Building a Defensible Audit Trail from Day One

The CRA doesn't accept vague summaries of exchange activity. They require detailed sub-ledgers for every corporate transaction, including the date, value in Canadian dollars, and the specific nature of the trade. Managing this complexity requires proactive oversight. Leveraging crypto CFO services during the formation phase helps you establish these systems before the volume of data becomes unmanageable. It's about building a system that turns raw blockchain data into a professional financial statement.

Documenting mining, staking, and DeFi rewards at the corporate level requires specialized methodology. Each reward is a taxable event under the Income Tax Act. Your accounting system must capture the fair market value of these tokens at the exact time of receipt. Without this granular data, your business remains vulnerable during a CRA audit. By establishing these protocols early, you ensure your venture is always audit-ready.

Reporting Foreign Property: The T1135 Requirement

Canadian corporations holding specified foreign property with a total cost of more than $100,000 at any time in the year must file Form T1135. For those pursuing crypto business incorporation canada, this frequently includes assets held on foreign exchanges or in decentralized protocols that the CRA considers "situated" outside of Canada. This reporting is mandatory regardless of whether the assets generated income during the year.

- Penalties: Failure to file can result in penalties of $25 per day, reaching a maximum of $2,500 per year, plus interest.

- Thresholds: The $100,000 limit applies to the total cost amount of all specified foreign property, not just crypto.

- Structure Impact: Your corporate hierarchy can influence how these thresholds are calculated across multiple entities.

Maintaining precise records of your specified foreign property isn't optional. It's a core requirement for staying compliant in a global digital economy. Strategic record-keeping ensures that you can accurately report these holdings and avoid the aggressive penalties associated with non-compliance.

Global reach is a hallmark of Web3, but it introduces significant friction with the CRA. Your strategy for crypto business incorporation canada must account for the fact that Canada taxes its residents on worldwide income. Founders often look to offshore jurisdictions to gain a competitive edge, yet without a sophisticated understanding of Foreign Accrual Property Income (FAPI) rules, these structures can lead to aggressive tax reassessments. If your foreign entity generates passive income, such as staking rewards or lending interest, that income may be taxed in Canada as it's earned, regardless of whether you bring the funds back to a Canadian bank account.

The CRA looks past the certificate of incorporation to determine where the "Mind and Management" of a company resides. If you're making key strategic decisions from your home in Ontario or British Columbia, the CRA may deem that foreign entity to be a Canadian resident for tax purposes. This creates a risk of double taxation if you haven't properly navigated the relevant tax treaties. For a deeper dive into these complex decisions, refer to our guide on choosing a jurisdiction for crypto business.

The Pitfalls of Unregulated Offshore Entities

The Multilateral Instrument (MLI) has fundamentally changed how tax treaties are applied, making it harder to use "tax-neutral" jurisdictions solely for tax avoidance. The CRA actively monitors for structures that lack economic substance. If your offshore entity doesn't have physical premises, local employees, or independent local management, the Canadian tax authorities will likely ignore the structure and tax the income at domestic rates. This reality makes the initial phase of crypto business incorporation canada critical; you must build a structure that stands up to international scrutiny and proves its operational independence.

Cross-Border Compliance in 2026

As we move into 2026, staying ahead of international crypto tax compliance standards is a prerequisite for survival. The implementation of the Crypto-Asset Reporting Framework (CARF) means that tax authorities worldwide are sharing data with unprecedented speed. For multi-jurisdictional Web3 firms, documenting transfer pricing is no longer optional. You must establish the rates at which different branches of your company charge each other for services to provide a vital defense against double taxation and transfer pricing penalties.

Managing global teams requires a disciplined approach to payroll and contractor payments. Paying contributors in stablecoins or native tokens still triggers reporting requirements for CRA filers. You need a framework that reconciles these payments with your corporate ledger to ensure you aren't inadvertently creating an unrecorded tax liability. Mastering these nuances allows you to manage cross-border crypto tax efficiently while maintaining a lean, global operation. Ready to secure your global structure? Contact our strategy team today to align your international operations with CRA standards.

Designing a Defensible Framework with Block3 Finance

Block3 Finance operates at the intersection of traditional fiscal discipline and decentralized innovation. We don't merely facilitate crypto business incorporation canada; we architect a financial system that supports your long-term vision. Our methodology ensures that your legal entity is perfectly synchronized with your wallet architecture, preventing the accounting friction that typically derails high-growth startups. By bridging the gap between legal formation and financial execution, we transform your corporate structure into a strategic asset that withstands the most rigorous CRA audits.

Customized Corporate Structuring for Web3

Different Web3 models require distinct financial blueprints. Whether you are launching a DeFi protocol, managing a DAO treasury, or scaling an NFT marketplace, your entity must reflect your operational reality. We specialize in implementing crypto to fiat payment solutions that allow your team to move capital with confidence. This integration is essential for managing daily operational expenses and ensuring that your on-chain activity translates seamlessly into your corporate books.

Our team acts as your primary partner for crypto accounting in Ontario, providing the local expertise needed to navigate provincial tax nuances alongside federal requirements. Engaging a specialized crypto tax accountant in Canada during the formation phase ensures your books are audit-ready from day one. We focus on creating a defensible record of every transaction, ensuring that your on and off-ramp solutions are fully integrated into your financial reporting framework.

Your Roadmap to Compliance

The journey toward a compliant, scalable crypto venture begins with a comprehensive assessment of your business model and jurisdictional requirements. We evaluate your director residency, treasury goals, and cross-border needs to recommend the most tax-efficient path for crypto business incorporation canada. As your firm scales, we provide continuous monitoring of evolving digital asset tax standards, ensuring you remain ahead of 2026 reporting mandates like the Crypto-Asset Reporting Framework (CARF). To ensure your broader operational logistics are just as organized as your taxes, you can learn more about managing road test scheduling for your team's licensing needs.

Success in the digital asset space requires a partner who understands that vision and execution are inseparable. We move beyond defensive compliance to help you gain total command over your financial landscape. This proactive stance allows you to shift from merely managing regulations to focusing on mastery and growth. To begin your structuring journey and secure your venture's future, contact our executive team for a strategic consultation.

Architecting Your Path to Global Scale

Building a sustainable venture in the digital asset space requires shifting from a defensive posture to an offensive strategy of mastery. We've explored how the right framework for crypto business incorporation canada transforms your on-chain activity into a defensible, tax-efficient record. By leveraging the CCPC advantage and proactively managing FAPI risks, you ensure your business remains resilient against CRA scrutiny while preserving capital for growth. For teams seeking further strategic guidance on execution, top7llc.com provides support to help organizations overcome common growth obstacles.

Block3 Finance brings 13 years of blockchain financial expertise and specialized Canadian tax knowledge to every engagement. Ranked as a top provider by Bitcoin.com and having served over 980 global clients, we bridge the gap between complex protocol mechanics and rigorous corporate governance. It's time to move beyond the uncertainty of raw data and claim total command over your financial landscape. Your vision deserves a foundation that's as innovative as the technology you're building.

For ventures requiring similar chartered expertise for their UK-based operations, you can check out Fair View Accounting Services to further bolster your international financial landscape.

Secure your crypto business’s future with expert corporate structuring from Block3 Finance.

Frequently Asked Questions

What is the most tax-efficient business structure for a Canadian crypto startup?

The Canadian-Controlled Private Corporation (CCPC) is generally the most tax-efficient structure for domestic startups due to the Small Business Deduction. Under CRA rules for 2026, CCPCs benefit from a reduced federal tax rate of 9% on the first $500,000 of active business income. This structure allows founders to reinvest profits at a significantly lower tax cost compared to personal marginal rates, which can exceed 50% in many provinces.

Can I use a Canadian-Controlled Private Corporation (CCPC) for my crypto mining business?

Crypto mining businesses are eligible for CCPC status because the CRA generally views mining as an active business rather than a passive investment. The high degree of operational activity, including hardware maintenance and software management, qualifies the income as active. As a CCPC, your mining operation can access the Small Business Deduction and potentially claim SR&ED tax credits for technical protocol developments performed within Canada. For businesses with significant equipment costs, staying informed on global tax trends like those discussed at businesswise.com.au can provide additional perspective on maximizing hardware-related deductions.

Does the CRA tax crypto profits in a corporation as business income or capital gains?

The CRA treats most corporate crypto profits as 100% taxable business income rather than capital gains. Classification depends on factors like transaction frequency, ownership period, and professional expertise. While individuals may access capital gains treatment, the CRA often presumes that a corporation's primary motive is profit generation, making active trading or mining fully taxable at the applicable corporate rate under the Income Tax Act.

Do I need to file a T1135 if my corporation holds crypto on a US-based exchange?

You must file Form T1135 if your corporation holds digital assets on a US-based exchange with a total cost exceeding $100,000 CAD at any point in the year. The CRA considers assets held on foreign exchanges as specified foreign property. Even if your crypto business incorporation canada is domestic, holding assets on foreign platforms triggers this mandatory reporting requirement, with significant daily penalties for non-compliance.

What are the risks of incorporating my crypto business in an offshore jurisdiction as a Canadian resident?

The greatest risk of offshore incorporation is the Foreign Accrual Property Income (FAPI) regime, which can trigger immediate Canadian taxation on passive earnings. Additionally, the "Mind and Management" rule allows the CRA to deem a foreign corporation as a Canadian resident if the directors make decisions while physically in Canada. This results in the entity being taxed on its worldwide income at standard Canadian corporate rates regardless of its registration.

How do I pay employees in crypto legally within a Canadian corporate structure?

Paying employees in digital assets is legal provided you treat the transaction as a benefit in kind under the Income Tax Act. You must calculate the fair market value of the tokens in Canadian dollars at the exact time of the transfer. The employer is responsible for remitting fiat-based payroll deductions, including income tax, CPP, and EI, to the CRA based on that converted value to ensure full compliance.

What happens if I don’t formalize my crypto business entity and continue as a sole proprietor?

Operating as a sole proprietor leaves you personally liable for protocol failures and subjects your profits to the highest personal tax brackets. Without a formal corporate veil, your personal assets are exposed to business-related lawsuits or smart contract vulnerabilities. Incorporating allows you to cap your tax liability at the 9% small business rate and creates a vital legal separation between your personal wealth and your venture.

Can a Canadian corporation claim the Small Business Deduction on crypto trading profits?

A corporation can claim the Small Business Deduction on crypto trading profits if the activity is classified as an active business. The CRA distinguishes between active business income and specified investment business income, which is taxed at higher rates. If your crypto business incorporation canada involves high-frequency trading or market making, you typically qualify for the 9% federal rate on the first $500,000 of income in 2026.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Block3 Finance, with over 26+ years of Canadian and international tax and accounting experience. A crypto accounting specialist since the early days of Bitcoin, he has consulted for over 38 crypto companies and collaborated with legal professionals on regulatory matters. His expertise spans corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, and CRA audits.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Block3 Finance and Tax Partners has 44 full-time accountants and over 9,800+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances.

Frequently Asked Questions

What is the most tax-efficient business structure for a Canadian crypto startup?

The Canadian-Controlled Private Corporation (CCPC) is generally the most tax-efficient structure for domestic startups due to the Small Business Deduction. Under CRA rules for 2026, CCPCs benefit from a reduced federal tax rate of 9% on the first $500,000 of active business income. This structure allows founders to reinvest profits at a significantly lower tax cost compared to personal marginal rates, which can exceed 50% in many provinces.

Can I use a Canadian-Controlled Private Corporation (CCPC) for my crypto mining business?

Crypto mining businesses are eligible for CCPC status because the CRA generally views mining as an active business rather than a passive investment. The high degree of operational activity, including hardware maintenance and software management, qualifies the income as active. As a CCPC, your mining operation can access the Small Business Deduction and potentially claim SR&ED tax credits for technical protocol developments performed within Canada.

Does the CRA tax crypto profits in a corporation as business income or capital gains?

The CRA treats most corporate crypto profits as 100% taxable business income rather than capital gains. Classification depends on factors like transaction frequency, ownership period, and professional expertise. While individuals may access capital gains treatment, the CRA often presumes that a corporation's primary motive is profit generation, making active trading or mining fully taxable at the applicable corporate rate under the Income Tax Act.

Do I need to file a T1135 if my corporation holds crypto on a US-based exchange?

You must file Form T1135 if your corporation holds digital assets on a US-based exchange with a total cost exceeding $100,000 CAD at any point in the year. The CRA considers assets held on foreign exchanges as specified foreign property. Even if your crypto business incorporation canada is domestic, holding assets on foreign platforms triggers this mandatory reporting requirement, with significant daily penalties for non-compliance.

What are the risks of incorporating my crypto business in an offshore jurisdiction as a Canadian resident?

The greatest risk of offshore incorporation is the Foreign Accrual Property Income (FAPI) regime, which can trigger immediate Canadian taxation on passive earnings. Additionally, the "Mind and Management" rule allows the CRA to deem a foreign corporation as a Canadian resident if the directors make decisions while physically in Canada. This results in the entity being taxed on its worldwide income at standard Canadian corporate rates regardless of its registration.

How do I pay employees in crypto legally within a Canadian corporate structure?

Paying employees in digital assets is legal provided you treat the transaction as a benefit in kind under the Income Tax Act. You must calculate the fair market value of the tokens in Canadian dollars at the exact time of the transfer. The employer is responsible for remitting fiat-based payroll deductions, including income tax, CPP, and EI, to the CRA based on that converted value to ensure full compliance.

What happens if I don’t formalize my crypto business entity and continue as a sole proprietor?

Operating as a sole proprietor leaves you personally liable for protocol failures and subjects your profits to the highest personal tax brackets. Without a formal corporate veil, your personal assets are exposed to business-related lawsuits or smart contract vulnerabilities. Incorporating allows you to cap your tax liability at the 9% small business rate and creates a vital legal separation between your personal wealth and your venture.

Can a Canadian corporation claim the Small Business Deduction on crypto trading profits?

A corporation can claim the Small Business Deduction on crypto trading profits if the activity is classified as an active business. The CRA distinguishes between active business income and specified investment business income, which is taxed at higher rates. If your crypto business incorporation canada involves high-frequency trading or market making, you typically qualify for the 9% federal rate on the first $500,000 of income in 2026.