The borderless nature of decentralized finance is a dangerous fallacy that tax authorities officially dismantled on January 1, 2026. You likely feel the mounting pressure of reporting requirements like CARF and DAC8, wondering if your offshore accounts or DeFi yields are about to trigger a cascade of audits across multiple jurisdictions. It's a rational concern. The fear of double taxation is a heavy burden when you're managing assets across a fragmented global landscape where definitions of property and currency seem to shift at every border.

We're here to replace that uncertainty with a sophisticated strategy for cross-border crypto tax compliance. You deserve to move from a defensive posture to one of absolute mastery over your financial destiny. This article debunks the most persistent myths regarding international digital asset taxation and provides the clear framework you need to determine tax nexus with precision. We'll verify which loopholes are actually liabilities and show you how to protect your global wealth with total confidence in your compliance strategy.

Key Takeaways

- Identify the specific tax nexus of your digital assets to dismantle the misconception that decentralized protocols exist outside the reach of physical jurisdictions.

- Navigate the mandatory transparency of CARF and DAC8 by understanding how automated data exchange between tax authorities impacts your reporting obligations in 2026.

- Protect your international portfolio from redundant liabilities by utilizing Double Tax Agreements and strategic credit methods to mitigate risks in a cross-border crypto tax environment.

- Resolve the "sourcing" problem for DeFi and NFTs by establishing a clear framework for determining which country holds the primary taxing rights over your transactions.

- Shift your approach from reactive filing to strategic wealth mastery by leveraging professional compliance standards and defensible on-chain financial records.

The "Borderless" Fallacy: Why Decentralization Does Not Equal Tax Immunity

The digital asset ecosystem often markets itself as a sovereign realm, existing entirely in the "ether" beyond the reach of traditional states. This is a dangerous fiction. While your private keys may be decentralized, your physical body and economic interests are not. Tax authorities have spent the last few years refining their reach, culminating in the 2026 reporting standards that effectively tether your on-chain activity to the ground you stand on. The cloud is a ghost; the law cares about the human at the keyboard. If you are physically present in a jurisdiction when you execute a trade, that "click" creates a footprint that most governments are now equipped to track.

Determining your cross-border crypto tax obligations begins with understanding the concept of Tax Nexus. Tax Nexus is the legal link between a taxpayer and a jurisdiction. For Web3 firms and decentralized teams, this often triggers the "Permanent Establishment" rule. If your core developers or executives operate from a specific country, that nation may claim taxing rights over the entire entity, regardless of where your foundation is incorporated. Mastery of these rules is the difference between strategic growth and catastrophic liability.

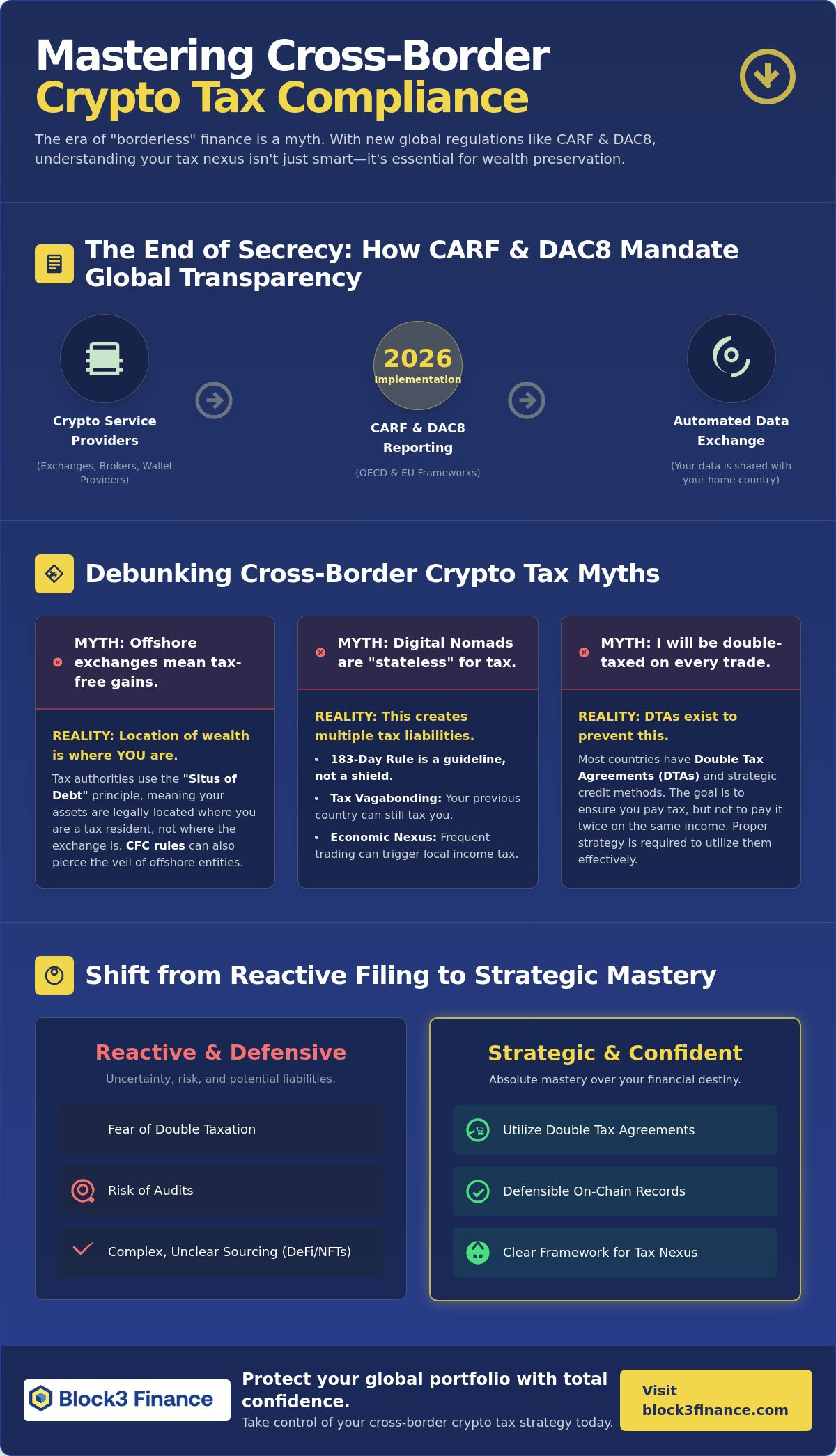

Myth: "If the Exchange is Offshore, the Gains are Tax-Free"

Many investors believe that holding assets on a platform based in a tax-neutral territory like the Seychelles or the British Virgin Islands grants them immunity. This ignores the "Situs of Debt" principle. Authorities generally view the location of your digital wealth as being wherever you, the owner, are tax-resident. Furthermore, modern anti-deferral regimes, such as Controlled Foreign Corporation (CFC) rules, are designed to pierce the veil of offshore entities. Understanding the Legality of cryptocurrency by country is essential, as local regulations will almost always override the perceived "offshore" status of a service provider.

The Digital Nomad Trap: Tax Residency vs. Physical Presence

The nomadic lifestyle creates a unique set of vulnerabilities for crypto-native professionals. You might assume that moving every 90 days keeps you "stateless," but tax authorities abhor a vacuum. If you don't establish a clear "Center of Vital Interests" in one specific country, multiple jurisdictions may attempt to claim you as a resident simultaneously. To protect your wealth, you must proactively manage these factors:

- The 183-Day Rule: While a common benchmark, many countries use "subjective ties" like bank accounts or housing to claim residency much sooner.

- Tax Vagabonding: Without a declared tax home, your previous country of residence often retains the right to tax your global cross-border crypto tax gains.

- Economic Nexus: High-frequency traders may be classified as "carrying on a trade" in a country even during a short stay, triggering local income tax instead of capital gains.

We help you navigate these high-stakes environments by shifting your posture from defensive management to offensive command. By establishing a defensible residency strategy, you turn a volatile regulatory landscape into a roadmap for global wealth preservation.

The End of Secrecy: How CARF and DAC8 Mandate Global Transparency

The era of "don't ask, don't tell" in digital finance has vanished. In its place stands a sophisticated web of automated surveillance designed to synchronize tax data across dozens of participating jurisdictions. The 2026 implementation of the OECD's Crypto-Asset Reporting Framework (CARF) and the EU's DAC8 directive marks the transition from manual audits to algorithmic enforcement. These frameworks don't just target centralized exchanges; they create a mandatory reporting loop for any entity providing crypto-asset services, including certain wallet providers and brokers.

Your KYC data from as far back as 2023 is already being shared with your home country. Many investors operate under the delusion that privacy coins or self-custody wallets provide a permanent shield against cross-border crypto tax scrutiny. This is a tactical error. While on-chain privacy exists, the entry and exit points are now heavily guarded. The chain of custody for your funds becomes transparent the moment it touches a regulated service provider or an off-ramp solution.

Automatic Exchange of Information (AEOI) for Digital Assets

The Common Reporting Standard (CRS) has evolved to encompass the complexities of the blockchain ecosystem. CARF requires service providers to report transactions annually to local authorities, who then swap that data with your country of residence automatically. Your activity in a foreign jurisdiction is no longer a localized event. It is a global broadcast. When you convert digital wealth into fiat or move assets through a regulated gateway, the transaction details often arrive at your tax office before you even file your return. Engaging in proactive Audits and Compliance ensures your reported data remains defensible and accurate.

Myth: "DAOs are Immune to Jurisdictional Reporting"

Decentralized Autonomous Organizations (DAOs) are often touted as the ultimate jurisdictional dodge. Regulators are rapidly dispelling this myth by piercing the "decentralized" veil to find responsible parties. In many cross-border disputes, authorities are assigning "Unincorporated Association" status to DAOs. This classification removes the shield of anonymity and places the tax burden directly on the contributors and participants. If you receive rewards, governance tokens, or yield from a DAO, you must track your "Global Source" income with surgical precision. Failing to do so invites an audit that treats your entire portfolio as high-risk, unclassified income. True mastery of your global wealth requires moving beyond the technical architecture of decentralization to address the practical realities of international law.

Myth: "I Will Be Double-Taxed on Every Cross-Border Trade"

The specter of paying taxes twice on the same gain is the primary deterrent for global digital asset participants. It is a rational fear, but often an unfounded one. Double Tax Agreements (DTAs) serve as the primary defense against this financial redundancy. These treaties exist to ensure that income is not taxed in both the country of source and the country of residence. In the context of cross-border crypto tax planning, the "Tie-Breaker" rule is your most potent tool. When two nations claim you as a resident, these rules provide a hierarchy of tests, such as permanent home, center of vital interests, and habitual abode, to determine which jurisdiction has the primary right to tax your global portfolio.

Most jurisdictions employ either the "Exemption" or "Credit" method to mitigate double taxation. The exemption method simply excludes foreign-sourced income from the domestic tax base. The credit method is more common for digital assets; it allows you to subtract the tax paid abroad from your local tax bill. However, crypto-to-crypto trades frequently create "phantom" liabilities. If Country A taxes a swap as a disposal but Country B does not recognize the event until a fiat exit, you risk timing mismatches that complicate your credit claims. Precision in your reporting timeline is the only way to resolve these jurisdictional conflicts.

Navigating Foreign Tax Credits (FTC) for Crypto

Claiming a Foreign Tax Credit on staking rewards requires meticulous execution. If you pay income tax on rewards in the country where the validator is located, your home country should theoretically offer a credit. The pitfall lies in "equivalence." Some authorities may not recognize a specific foreign levy as a "covered tax" under the treaty. You must maintain "Audit-Ready" books that clearly link every foreign payment to a specific on-chain event. This documentation is the only shield against a double-tax assessment during a cross-border inquiry. We help you build these defensible records to ensure your credits are never disqualified due to lack of evidence.

The Role of Bilateral Tax Treaties in Web3

Strategic navigation involves identifying which nations have established "Crypto-Friendly" treaties with your primary residence. These bilateral agreements often reduce withholding taxes on payments derived from digital asset services or corporate distributions. By aligning your operational footprint with these legal frameworks, you move from a defensive posture of survival to an offensive strategy of wealth optimization. Ensure your global structure is tax-efficient with Block3 Finance to maintain total command over your international liabilities. We provide the roadmap to turn complex treaty law into a tangible competitive advantage for your global wealth.

Sourcing the Unsourceable: Determining the Nexus of DeFi and NFTs

Traditional tax frameworks rely on the physical location of assets or parties to determine who gets a piece of the economic pie. Decentralized Finance (DeFi) and Non-Fungible Tokens (NFTs) dismantle this logic by operating in a distributed environment where the borrower, the lender, and the protocol itself may exist in three different hemispheres. Sourcing is the process of determining which country has the primary right to tax an income stream. In the context of cross-border crypto tax, this determination is no longer a theoretical exercise; it is a mandatory requirement for avoiding aggressive double-taxation or penalties for under-reporting.

We're seeing a decisive transition from "Residence-Based" to "Source-Based" taxation in global digital policy. While your home country usually taxes your global income, the country where the income "originates" often claims the first right of refusal. If a protocol is governed by a DAO with a heavy concentration of nodes or developers in a specific jurisdiction, that nation may argue the income is sourced within its borders. Defending your position in an audit requires a robust methodology for documenting "On-Chain Sourcing," proving that your yields or gains don't have a definitive nexus in a high-tax jurisdiction.

DeFi Liquidity Provisioning Across Borders

The yield you earn from liquidity pools doesn't always fit neatly into legacy categories like interest or dividends. Depending on the protocol's architecture, your returns might be classified as capital gains or even ordinary income. High-volume DeFi participants face an additional risk: being classified as having "Trade or Business" status in a foreign land. If your automated strategies interact frequently with a protocol that has a permanent establishment in another country, you could inadvertently trigger local filing requirements. We help you classify these streams correctly to ensure your global yield remains a tool for growth rather than a source of friction.

NFT Royalties and Intellectual Property Nexus

Many collectors believe the myth that NFTs are like physical art and are only taxed where the owner is located. The reality is far more complex. NFT royalties are increasingly viewed as "Royalties" under international tax treaties, which often carry specific withholding requirements. High-value collections and metaverse land create a "Digital Situs" problem; if the virtual land is tied to a specific corporate entity, the gains from its sale might be sourced to that entity's home. To mitigate these risks, sophisticated investors are moving toward Corporate Structuring solutions that place NFT holdings within international entities designed for maximum protection. This proactive approach turns a chaotic digital landscape into a structured, defensible portfolio that stands up to global scrutiny.

Strategic Global Compliance: The Block3 Finance Advantage

The transition from survival to mastery requires more than just reactive accounting. Most market participants approach cross-border crypto tax with a sense of dread, viewing compliance as a hurdle to be cleared rather than a strategic asset to be cultivated. We reject this defensive posture. True wealth preservation in a borderless economy demands an offensive strategy, one that utilizes a Global Tax Roadmap to navigate the friction of conflicting jurisdictions. By integrating professional corporate structuring, we dismantle the myths of jurisdictional risk and replace them with a robust, defensible framework for your global digital operations.

Block3 Finance brings 13+ years of specialized on-chain expertise to the table. We don't just observe the blockchain ecosystem; we've been active participants in its evolution since the early days of decentralized finance. This deep immersion allows us to turn chaotic transaction histories into clean, institutional-grade financial records that satisfy the most rigorous audit standards. Our goal is to move you from the stress of "Defensive Filing" to the liberation of "Strategic Wealth Mastery" on a global scale.

Turning Complex On-Chain Data into Defensible Books

Reconciling multi-jurisdictional wallets and exchanges is a high-stakes puzzle that demands technical rigor. Our methodology focuses on the resolution of friction between disparate data sources, ensuring every on-ramp, off-ramp, and cross-chain swap is accounted for with surgical precision. As the reality of CARF and automated global audits becomes the standard in 2026, having a verified trail of activity is your only protection against aggressive enforcement. We prepare you for this transparent era by building books that aren't just accurate, but defensible. Learn about our International Crypto Tax Compliance services to secure your financial legacy.

Your Visionary Navigator in a Borderless Economy

A traditional accountant looks at where you've been; a Block3 CFO looks at where you're going. We position our CFO Services as the elite strategy layer for your global digital operations. This is white-glove corporate finance designed for the high-growth firms and founders who define the Web3 space. We provide the intellectual leadership and technical oversight necessary to thrive in a volatile landscape, offering a calm force amidst regulatory chaos. You gain total command over your international liabilities, shifting the narrative from managing regulations to mastering growth. Schedule a consultation with the top-ranked crypto tax firm today to begin your journey toward strategic wealth mastery.

Master Your Global Financial Footprint

The 2026 regulatory landscape has permanently altered the mechanics of international wealth. You've seen how the implementation of CARF and DAC8 has replaced the "borderless" myth with a regime of automated transparency; you've also learned how the strategic application of double tax agreements can neutralize the threat of redundant liabilities. Mastery of cross-border crypto tax is no longer a luxury but a fundamental requirement for anyone operating at the intersection of traditional finance and decentralized protocols. By correctly sourcing your DeFi yields and establishing a defensible tax nexus, you transform regulatory friction into a structured roadmap for growth.

Block3 Finance stands as your elite strategist in this complex environment. Top-ranked by Bitcoin.com and backed by 13+ years of blockchain financial expertise, we've successfully managed 980+ global clients through high-stakes compliance cycles. We provide the technical rigor and visionary oversight necessary to protect your assets across every jurisdiction you touch. Secure Your Global Crypto Wealth with Block3 Finance and gain total command over your financial destiny. The future of finance belongs to those who navigate with precision and foresight.

Frequently Asked Questions

Do I have to pay tax if I am a digital nomad with no fixed residence?

Yes, you generally remain liable for taxes even without a fixed physical home. Most jurisdictions apply residency tests that don't require a permanent address to claim you as a taxpayer. If you are a U.S. citizen, you are taxed on your global income regardless of where you rest your head. For others, your previous country of residence often retains taxing rights until you legally establish a "center of vital interests" elsewhere. Statelessness is a myth that tax authorities have effectively dismantled.

How does the IRS know about my trades on a foreign exchange like Binance or OKX?

The IRS gains visibility through the 2026 implementation of CARF and existing data-sharing frameworks like FATCA. Major international exchanges now collect Tax Identification Numbers (TINs) as part of their mandatory compliance protocols. This data is reported to local tax authorities, who then share it with the IRS through automated exchange programs. Your cross-border crypto tax footprint is much more visible than it was even two years ago.

Can I use a Double Tax Agreement (DTA) to pay zero tax on my crypto?

Double Tax Agreements are designed to prevent redundant taxation, not to eliminate your tax liability entirely. A DTA typically ensures you pay the higher of the two countries' tax rates by granting a credit for taxes already paid in the source country. While these treaties are powerful tools for wealth preservation, they aren't a loophole for total tax avoidance. They simply ensure you don't pay more than the single highest rate applicable to your situation.

What is the "CARF" regulation and how does it affect me in 2026?

The Crypto-Asset Reporting Framework (CARF) is an OECD-led initiative that mandates the automatic exchange of information between 47 participating jurisdictions. Starting in 2026, crypto-asset service providers must report transaction data and user identities to their local authorities annually. This information is then broadcast to the tax office in your country of residence. It marks the definitive end of jurisdictional secrecy for digital asset holders.

Is moving to a "tax haven" like Dubai or Puerto Rico a valid cross-border strategy?

Relocating to a low-tax jurisdiction is a valid strategy, but it requires a total shift of your economic and personal life. For U.S. citizens moving to Puerto Rico, you must strictly satisfy the physical presence and "closer connection" tests under Act 60. In Dubai, you must ensure you've severed enough ties with your home country to prevent them from claiming you are still a resident. Simple "paper" residency is no longer a defensible strategy in 2026.

What happens if two countries both claim I am a tax resident?

You must invoke the "Tie-Breaker" rules found in the bilateral tax treaty between the two nations. These rules follow a strict hierarchy, looking first at where you have a permanent home, then your center of vital interests, and finally your habitual abode. Resolving these conflicts requires a sophisticated cross-border crypto tax defense to ensure you aren't taxed on your global portfolio by two different governments simultaneously.

Do I need to report my self-custody hardware wallets to foreign tax authorities?

You generally don't report the physical device, but you must report the income and assets associated with the addresses you control. While self-custody offers technical privacy, the moment your assets touch a regulated off-ramp or exchange, they enter the global reporting web. Many countries now require the disclosure of "foreign financial assets," which can include crypto held in private wallets if the value exceeds specific thresholds.

How do I claim a Foreign Tax Credit for crypto staking rewards earned abroad?

To claim a Foreign Tax Credit (FTC), you must first document that you paid a covered tax on that specific income to a foreign government. You then report the gross income on your domestic tax return and apply for a credit to offset your local liability. The primary challenge is proving "equivalence," as your home country must recognize the foreign levy as a valid income tax. Maintaining clean, audit-ready books is the only way to ensure these credits are accepted.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Block3 Finance, with over 26+ years of Canadian and international tax and accounting experience. A crypto accounting specialist since the early days of Bitcoin, he has consulted for over 38 crypto companies and collaborated with legal professionals on regulatory matters. His expertise spans corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, and CRA audits.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Block3 Finance and Tax Partners has 44 full-time accountants and over 9,800+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances.

Frequently Asked Questions

Myth: "If the Exchange is Offshore, the Gains are Tax-Free"

Many investors believe that holding assets on a platform based in a tax-neutral territory like the Seychelles or the British Virgin Islands grants them immunity. This ignores the "Situs of Debt" principle. Authorities generally view the location of your digital wealth as being wherever you, the owner, are tax-resident. Furthermore, modern anti-deferral regimes, such as Controlled Foreign Corporation (CFC) rules, are designed to pierce the veil of offshore entities. Understanding the Legality of cryptocurrency by country is essential, as local regulations will almost always override the perceived "offshore" status of a service provider.

The Digital Nomad Trap: Tax Residency vs. Physical Presence

The nomadic lifestyle creates a unique set of vulnerabilities for crypto-native professionals. You might assume that moving every 90 days keeps you "stateless," but tax authorities abhor a vacuum. If you don't establish a clear "Center of Vital Interests" in one specific country, multiple jurisdictions may attempt to claim you as a resident simultaneously. To protect your wealth, you must proactively manage these factors: We help you navigate these high-stakes environments by shifting your posture from defensive management to offensive command. By establishing a defensible residency strategy, you turn a volatile regulatory landscape into a roadmap for global wealth preservation. The era of "don't ask, don't tell" in digital finance has vanished. In its place stands a sophisticated web of automated surveillance designed to synchronize tax data across dozens of participating jurisdictions. The 2026 implementation of the OECD's Crypto-Asset Reporting Framework (CARF) and the EU's DAC8 directive marks the transition from manual audits to algorithmic enforcement. These frameworks don't just target centralized exchanges; they create a mandatory reporting loop for any entity providing crypto-asset services, including certain wallet providers and brokers. Your KYC data from as far back as 2023 is already being shared with your home country. Many investors operate under the delusion that privacy coins or self-custody wallets provide a permanent shield against cross-border crypto tax scrutiny. This is a tactical error. While on-chain privacy exists, the entry and exit points are now heavily guarded. The chain of custody for your funds becomes transparent the moment it touches a regulated service provider or an off-ramp solution.

Automatic Exchange of Information (AEOI) for Digital Assets

The Common Reporting Standard (CRS) has evolved to encompass the complexities of the blockchain ecosystem. CARF requires service providers to report transactions annually to local authorities, who then swap that data with your country of residence automatically. Your activity in a foreign jurisdiction is no longer a localized event. It is a global broadcast. When you convert digital wealth into fiat or move assets through a regulated gateway, the transaction details often arrive at your tax office before you even file your return. Engaging in proactive Audits and Compliance ensures your reported data remains defensible and accurate.

Myth: "DAOs are Immune to Jurisdictional Reporting"

Decentralized Autonomous Organizations (DAOs) are often touted as the ultimate jurisdictional dodge. Regulators are rapidly dispelling this myth by piercing the "decentralized" veil to find responsible parties. In many cross-border disputes, authorities are assigning "Unincorporated Association" status to DAOs. This classification removes the shield of anonymity and places the tax burden directly on the contributors and participants. If you receive rewards, governance tokens, or yield from a DAO, you must track your "Global Source" income with surgical precision. Failing to do so invites an audit that treats your entire portfolio as high-risk, unclassified income. True mastery of your global wealth requires moving beyond the technical architecture of decentralization to address the practical realities of international law. The specter of paying taxes twice on the same gain is the primary deterrent for global digital asset participants. It is a rational fear, but often an unfounded one. Double Tax Agreements (DTAs) serve as the primary defense against this financial redundancy. These treaties exist to ensure that income is not taxed in both the country of source and the country of residence. In the context of cross-border crypto tax planning, the "Tie-Breaker" rule is your most potent tool. When two nations claim you as a resident, these rules provide a hierarchy of tests, such as permanent home, center of vital interests, and habitual abode, to determine which jurisdiction has the primary right to tax your global portfolio. Most jurisdictions employ either the "Exemption" or "Credit" method to mitigate double taxation. The exemption method simply excludes foreign-sourced income from the domestic tax base. The credit method is more common for digital assets; it allows you to subtract the tax paid abroad from your local tax bill. However, crypto-to-crypto trades frequently create "phantom" liabilities. If Country A taxes a swap as a disposal but Country B does not recognize the event until a fiat exit, you risk timing mismatches that complicate your credit claims. Precision in your reporting timeline is the only way to resolve these jurisdictional conflicts.

Navigating Foreign Tax Credits (FTC) for Crypto

Claiming a Foreign Tax Credit on staking rewards requires meticulous execution. If you pay income tax on rewards in the country where the validator is located, your home country should theoretically offer a credit. The pitfall lies in "equivalence." Some authorities may not recognize a specific foreign levy as a "covered tax" under the treaty. You must maintain "Audit-Ready" books that clearly link every foreign payment to a specific on-chain event. This documentation is the only shield against a double-tax assessment during a cross-border inquiry. We help you build these defensible records to ensure your credits are never disqualified due to lack of evidence.

The Role of Bilateral Tax Treaties in Web3

Strategic navigation involves identifying which nations have established "Crypto-Friendly" treaties with your primary residence. These bilateral agreements often reduce withholding taxes on payments derived from digital asset services or corporate distributions. By aligning your operational footprint with these legal frameworks, you move from a defensive posture of survival to an offensive strategy of wealth optimization. Ensure your global structure is tax-efficient with Block3 Finance to maintain total command over your international liabilities. We provide the roadmap to turn complex treaty law into a tangible competitive advantage for your global wealth. Traditional tax frameworks rely on the physical location of assets or parties to determine who gets a piece of the economic pie. Decentralized Finance (DeFi) and Non-Fungible Tokens (NFTs) dismantle this logic by operating in a distributed environment where the borrower, the lender, and the protocol itself may exist in three different hemispheres. Sourcing is the process of determining which country has the primary right to tax an income stream. In the context of cross-border crypto tax, this determination is no longer a theoretical exercise; it is a mandatory requirement for avoiding aggressive double-taxation or penalties for under-reporting. We're seeing a decisive transition from "Residence-Based" to "Source-Based" taxation in global digital policy. While your home country usually taxes your global income, the country where the income "originates" often claims the first right of refusal. If a protocol is governed by a DAO with a heavy concentration of nodes or developers in a specific jurisdiction, that nation may argue the income is sourced within its borders. Defending your position in an audit requires a robust methodology for documenting "On-Chain Sourcing," proving that your yields or gains don't have a definitive nexus in a high-tax jurisdiction.

DeFi Liquidity Provisioning Across Borders

The yield you earn from liquidity pools doesn't always fit neatly into legacy categories like interest or dividends. Depending on the protocol's architecture, your returns might be classified as capital gains or even ordinary income. High-volume DeFi participants face an additional risk: being classified as having "Trade or Business" status in a foreign land. If your automated strategies interact frequently with a protocol that has a permanent establishment in another country, you could inadvertently trigger local filing requirements. We help you classify these streams correctly to ensure your global yield remains a tool for growth rather than a source of friction.

NFT Royalties and Intellectual Property Nexus

Many collectors believe the myth that NFTs are like physical art and are only taxed where the owner is located. The reality is far more complex. NFT royalties are increasingly viewed as "Royalties" under international tax treaties, which often carry specific withholding requirements. High-value collections and metaverse land create a "Digital Situs" problem; if the virtual land is tied to a specific corporate entity, the gains from its sale might be sourced to that entity's home. To mitigate these risks, sophisticated investors are moving toward Corporate Structuring solutions that place NFT holdings within international entities designed for maximum protection. This proactive approach turns a chaotic digital landscape into a structured, defensible portfolio that stands up to global scrutiny. The transition from survival to mastery requires more than just reactive accounting. Most market participants approach cross-border crypto tax with a sense of dread, viewing compliance as a hurdle to be cleared rather than a strategic asset to be cultivated. We reject this defensive posture. True wealth preservation in a borderless economy demands an offensive strategy, one that utilizes a Global Tax Roadmap to navigate the friction of conflicting jurisdictions. By integrating professional corporate structuring, we dismantle the myths of jurisdictional risk and replace them with a robust, defensible framework for your global digital operations. Block3 Finance brings 13+ years of specialized on-chain expertise to the table. We don't just observe the blockchain ecosystem; we've been active participants in its evolution since the early days of decentralized finance. This deep immersion allows us to turn chaotic transaction histories into clean, institutional-grade financial records that satisfy the most rigorous audit standards. Our goal is to move you from the stress of "Defensive Filing" to the liberation of "Strategic Wealth Mastery" on a global scale.

Turning Complex On-Chain Data into Defensible Books

Reconciling multi-jurisdictional wallets and exchanges is a high-stakes puzzle that demands technical rigor. Our methodology focuses on the resolution of friction between disparate data sources, ensuring every on-ramp, off-ramp, and cross-chain swap is accounted for with surgical precision. As the reality of CARF and automated global audits becomes the standard in 2026, having a verified trail of activity is your only protection against aggressive enforcement. We prepare you for this transparent era by building books that aren't just accurate, but defensible. Learn about our International Crypto Tax Compliance services to secure your financial legacy.

Your Visionary Navigator in a Borderless Economy

A traditional accountant looks at where you've been; a Block3 CFO looks at where you're going. We position our CFO Services as the elite strategy layer for your global digital operations. This is white-glove corporate finance designed for the high-growth firms and founders who define the Web3 space. We provide the intellectual leadership and technical oversight necessary to thrive in a volatile landscape, offering a calm force amidst regulatory chaos. You gain total command over your international liabilities, shifting the narrative from managing regulations to mastering growth. Schedule a consultation with the top-ranked crypto tax firm today to begin your journey toward strategic wealth mastery. The 2026 regulatory landscape has permanently altered the mechanics of international wealth. You've seen how the implementation of CARF and DAC8 has replaced the "borderless" myth with a regime of automated transparency; you've also learned how the strategic application of double tax agreements can neutralize the threat of redundant liabilities. Mastery of cross-border crypto tax is no longer a luxury but a fundamental requirement for anyone operating at the intersection of traditional finance and decentralized protocols. By correctly sourcing your DeFi yields and establishing a defensible tax nexus, you transform regulatory friction into a structured roadmap for growth. Block3 Finance stands as your elite strategist in this complex environment. Top-ranked by Bitcoin.com and backed by 13+ years of blockchain financial expertise, we've successfully managed 980+ global clients through high-stakes compliance cycles. We provide the technical rigor and visionary oversight necessary to protect your assets across every jurisdiction you touch. Secure Your Global Crypto Wealth with Block3 Finance and gain total command over your financial destiny. The future of finance belongs to those who navigate with precision and foresight.

Do I have to pay tax if I am a digital nomad with no fixed residence?

Yes, you generally remain liable for taxes even without a fixed physical home. Most jurisdictions apply residency tests that don't require a permanent address to claim you as a taxpayer. If you are a U.S. citizen, you are taxed on your global income regardless of where you rest your head. For others, your previous country of residence often retains taxing rights until you legally establish a "center of vital interests" elsewhere. Statelessness is a myth that tax authorities have effectively dismantled.

How does the IRS know about my trades on a foreign exchange like Binance or OKX?

The IRS gains visibility through the 2026 implementation of CARF and existing data-sharing frameworks like FATCA. Major international exchanges now collect Tax Identification Numbers (TINs) as part of their mandatory compliance protocols. This data is reported to local tax authorities, who then share it with the IRS through automated exchange programs. Your cross-border crypto tax footprint is much more visible than it was even two years ago.

Can I use a Double Tax Agreement (DTA) to pay zero tax on my crypto?

Double Tax Agreements are designed to prevent redundant taxation, not to eliminate your tax liability entirely. A DTA typically ensures you pay the higher of the two countries' tax rates by granting a credit for taxes already paid in the source country. While these treaties are powerful tools for wealth preservation, they aren't a loophole for total tax avoidance. They simply ensure you don't pay more than the single highest rate applicable to your situation.

What is the "CARF" regulation and how does it affect me in 2026?

The Crypto-Asset Reporting Framework (CARF) is an OECD-led initiative that mandates the automatic exchange of information between 47 participating jurisdictions. Starting in 2026, crypto-asset service providers must report transaction data and user identities to their local authorities annually. This information is then broadcast to the tax office in your country of residence. It marks the definitive end of jurisdictional secrecy for digital asset holders.

Is moving to a "tax haven" like Dubai or Puerto Rico a valid cross-border strategy?

Relocating to a low-tax jurisdiction is a valid strategy, but it requires a total shift of your economic and personal life. For U.S. citizens moving to Puerto Rico, you must strictly satisfy the physical presence and "closer connection" tests under Act 60. In Dubai, you must ensure you've severed enough ties with your home country to prevent them from claiming you are still a resident. Simple "paper" residency is no longer a defensible strategy in 2026.

What happens if two countries both claim I am a tax resident?

You must invoke the "Tie-Breaker" rules found in the bilateral tax treaty between the two nations. These rules follow a strict hierarchy, looking first at where you have a permanent home, then your center of vital interests, and finally your habitual abode. Resolving these conflicts requires a sophisticated cross-border crypto tax defense to ensure you aren't taxed on your global portfolio by two different governments simultaneously.

Do I need to report my self-custody hardware wallets to foreign tax authorities?

You generally don't report the physical device, but you must report the income and assets associated with the addresses you control. While self-custody offers technical privacy, the moment your assets touch a regulated off-ramp or exchange, they enter the global reporting web. Many countries now require the disclosure of "foreign financial assets," which can include crypto held in private wallets if the value exceeds specific thresholds.

How do I claim a Foreign Tax Credit for crypto staking rewards earned abroad?

To claim a Foreign Tax Credit (FTC), you must first document that you paid a covered tax on that specific income to a foreign government. You then report the gross income on your domestic tax return and apply for a credit to offset your local liability. The primary challenge is proving "equivalence," as your home country must recognize the foreign levy as a valid income tax. Maintaining clean, audit-ready books is the only way to ensure these credits are accepted.